Will Saudi Arabia and Russia agree on production cuts to save oil market?

Published on 08 Apr, 2020

Oil prices are gyrating due to the delay in Saudi Arabia and Russia reaching an agreement on cutting production. In a hostile environment, amid oversupply and falling demand, oil prices have become extremely volatile. Due to the pandemic and resultant shutdowns, demand has taken a hit, but market conditions for oil were challenging even in pre-COVID-19 days. With no respite from lockdowns in near future, oil storage facilities may reach capacity soon and logistics would become expensive for producers. Prospects, therefore, hinge on Russia and Saudi Arabia reaching an agreement soon. Expect prices to remain skewed downwards for some more time.

Oil prices are again weak after last week’s late rally. This was expected as news came in that a likely discussion between Saudi Arabia and Russia, planned for Monday April 06, had been pushed to Thursday, April 09. Further news emerged of an emergency meeting of oil ministers of G20 countries being called on Friday, April 10. Reacting to these developments, oil prices have turned volatile and will react sharply to any speculation until a concrete and executable plan emerges soon.

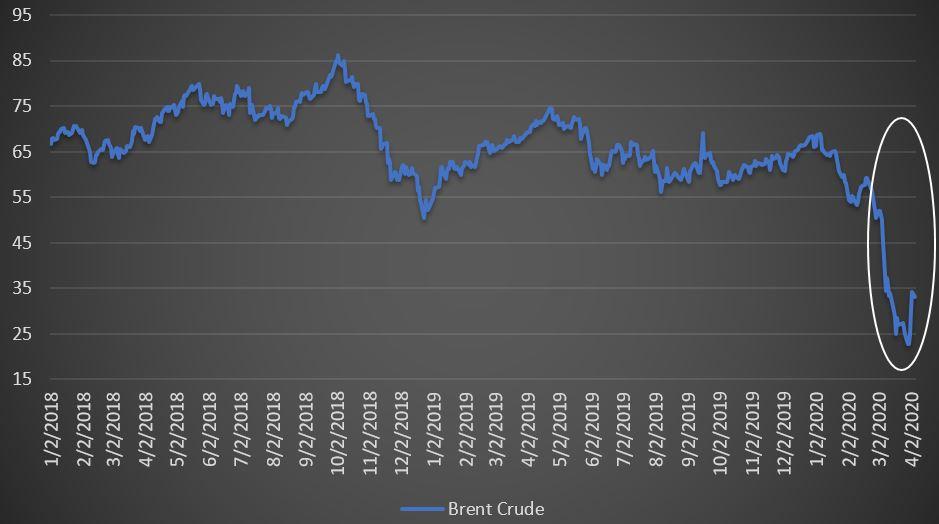

Exhibit 1: Sharp fall in oil prices in March 2020 (USD/bl)

Source: Reuters Eikon

Currently, demand is severely restricted. Going by estimates provided by the Chief Economist at trading firm Trafigura, the daily global demand would decrease by as much as 30mbpd or about one-third due to the lockdowns across the world. In 2019, oil prices were already under pressure amid decelerating global growth and slowdown in major consumer markets such as China. Hence, even after the world recovers from this epidemic, the timeline for which is highly uncertain, demand for oil would remain subdued.

In the past two years, the only support for oil price was to adjust supply as per demand. Since production is spread across OPEC and many other producers, they needed to agree on curbing it. This was attempted successfully in 2018 and 2019 by OPEC and select non-OPEC producers, including Russia, when nearly all producers in the group adhered to a set production amount as per mutually agreed quotas. Some producers like Russia fell behind in cutting production, but Saudi Arabia more than made up for the gap by cutting more than its quota. However, this arrangement did not include the world’s largest producer, the US. Competition laws prevent US producers from being part of any such agreement, lest they are directed by their local states to curtail production. The federal government does not have much say in this matter and leaves the market to be governed by demand and supply. This was confirmed last week based on what the US President had to say after his meeting with oil market executives.

The agreement between OPEC+ group of producers ended amid discord in March 2020; producers were now free to increase production, which removed the very support that had propped oil prices until now. Hence, it was not surprising that prices collapsed by over 50% in March. The only solution now is to once again reach an agreement to cut output which, however, looks difficult, considering the acrimony between the top producers, Saudi Arabia and Russia. Going by public comments from officials of both countries after the production-cut agreement ended, the two are not on the best of terms. Nevertheless, both countries are aware of the importance of keeping discussions alive for mutual benefit, and hence, the attempts to reinitiate talks. This time, Saudi Arabia has invited the Texas Commission to the discussion. The State of Texas, with many shale oilfields, is a key stakeholder and has the authority to direct producers to cut output. It can also act independently without attracting any action as per competition laws, by virtue of being a government body, unlike the other two industry associations: the US Oil & Gas Association and Independent Petroleum Association of America.

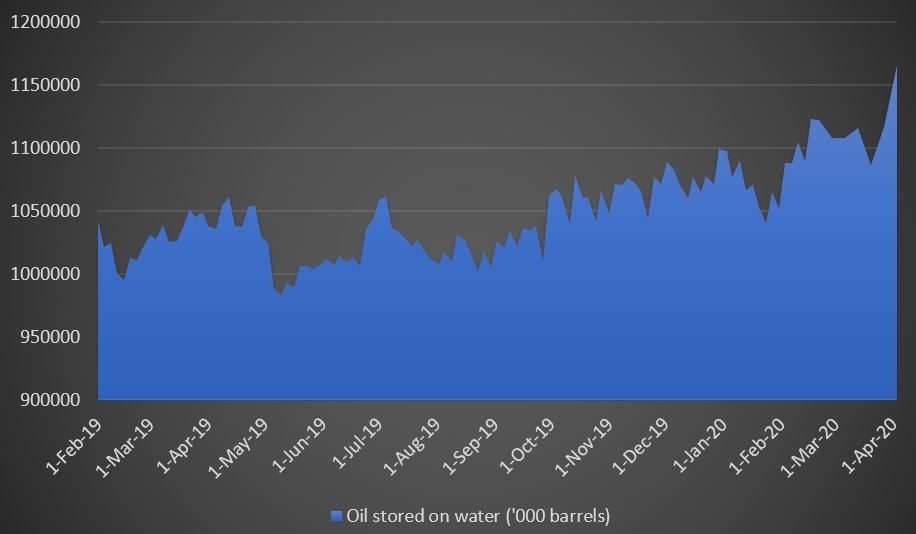

Warehousing the increasing supply of oil is another bomb that is ticking away, as storage is limited. Top storage facilities, such as those in the Emirate of Fujairah, are running out of capacity and expected to be filled up within a short span of few weeks. Even the US, which initially purchased oil for filling up strategic reserves, has ceased to do so. Oil data analytics firm Oiix has estimated that oil storage around the world could reach 1 billion barrels soon. Sources from shipping industry estimate that as much as 80 million barrels of oil are being stored in floating vessels around the world. If the world runs out of storage space, all producers will be forced to cut production with or without a deal. Indeed, as per media reports, at least 900,000 barrels per day of production in the US have been curtailed by "shut-ins".

Exhibit 2: Sharp rise in stored oil in March 2020 as demand falls but supply increases

Source: Bloomberg

This extreme situation has forced some producers to pay for transportation of oil sold to refineries, effectively meaning that certain varieties of oil (e.g. Wyoming Asphalt Sour) are being sold at negative rates, or sellers are paying buyers. The situation is especially severe for producers that are inland and have landlocked pipelines, like those in the US, Canada and Russia. Goldman Sachs estimates that WTI benchmark prices may even go negative as a result of the constraints mentioned above. The scenario is not very different downstream, as refineries also find that offtake for petrochemicals is falling in a world affected by the global slowdown. As refineries run out in terms of capacity, especially for those with older, less productive oil wells as the source of feedstock, the oil pumped out will literally have nowhere to go with regard to either usage or storage. Amid the supply glut and rising demand for storage, storage costs are spiraling. Research firm JBC Energy estimates that such ‘no-use’ crude would be around 6 million barrels per day in April and reach 7 million barrels per day soon.

Eventually, the epidemic will subside, economic activities will resume, and transportation and industrial demand for oil will increase, although the timeline remains uncertain. However, until then, oil markets would remain subdued, with small spikes whenever some positive news surfaces. All eyes are on Saudi Arabia and Russia – whether they will agree to return to negotiations and how soon. Saudi Arabia has demonstrated its inclination to production cuts and taken leadership position in cutting more than its quota in the past. Other oil producers, except Russia, have mostly followed Saudi Arabia in compliance. However, it will be critical to see whether Russia will agree to any production cuts, and given the recent acrimony, will Saudi Arabia be keen on holding talks again. The rescheduling of discussions from Monday to Thursday is just a short delay, but what is important is that the oil market has comprehended the challenge in getting the two parties to the table and reacted accordingly. Expect prices to remain skewed downwards for some more time.