The Unending Vodafone Idea Crisis: A Battle for SurVival

Published on 23 Jun, 2025

Despite multiple interventions, Vodafone Idea remains trapped in a cycle of high debt, regulatory overhang, and underinvestment. With dwindling subscriber share and a growing capex gap versus rivals Jio and Airtel, Vi’s future as a competitive player in India’s telecom sector hinges on urgent funding clarity and relief on AGR liabilities.

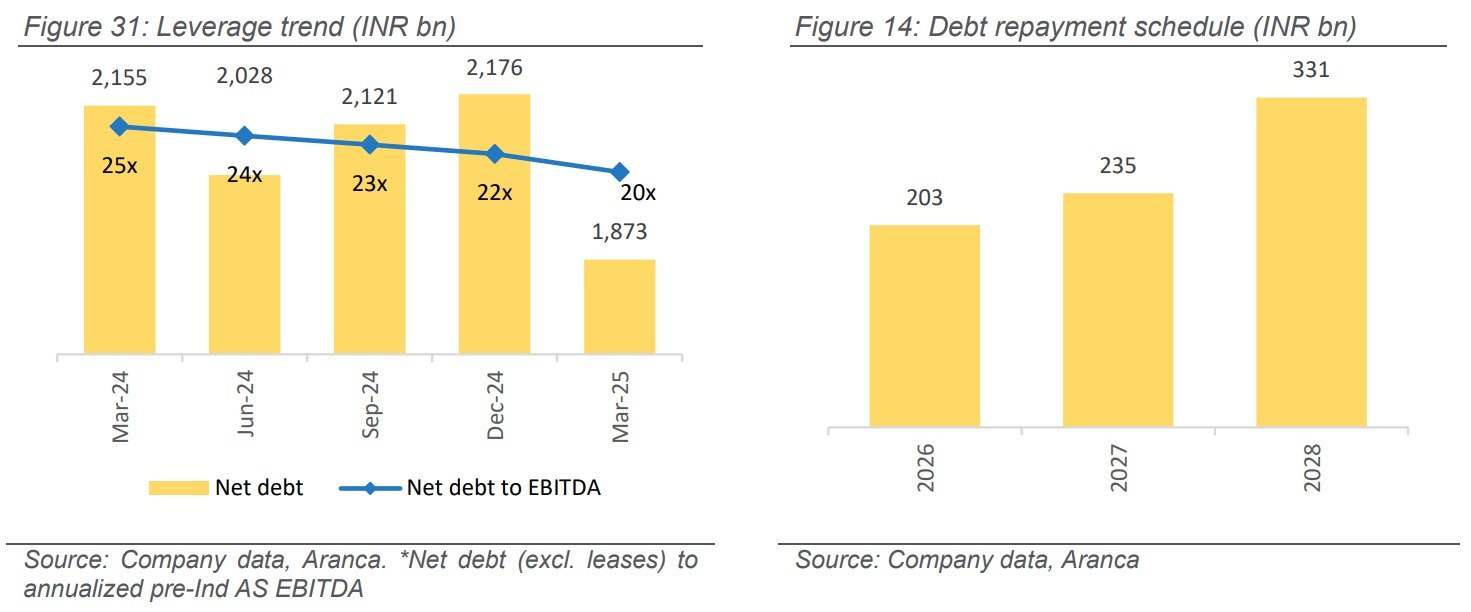

Vodafone Idea Limited (Vi), India's third-largest telecom operator (incorporated in 2018 via the Vodafone India-Idea Cellular merger), faces a deepening, protracted financial crisis. The company is critically burdened with a massive debt load (as of March 2025: INR 1,873 bn net debt; net debt (ex-leases) to annualized EBITDA is 20x) and persistent regulatory issues, particularly related to adjusted gross revenue (AGR) dues (~INR760bn). The financial stress has plagued the company over several years. Despite prolonged survival efforts, Vi recently indicated that it might not sustain operations beyond FY26 without immediate financial support and government relief on AGR dues.

Factors leading to the crisis

Declining market share amidst fierce competition

Vi continues to lose market share in India’s highly competitive telecom sector, reflecting a sustained decline in its operational viability. A detailed comparison of Vi's performance with that of Airtel and Reliance Jio—using key KPIs such as wireless subscriber base, wireless revenue market share, and ARPU—underscores Vi's vulnerable position.

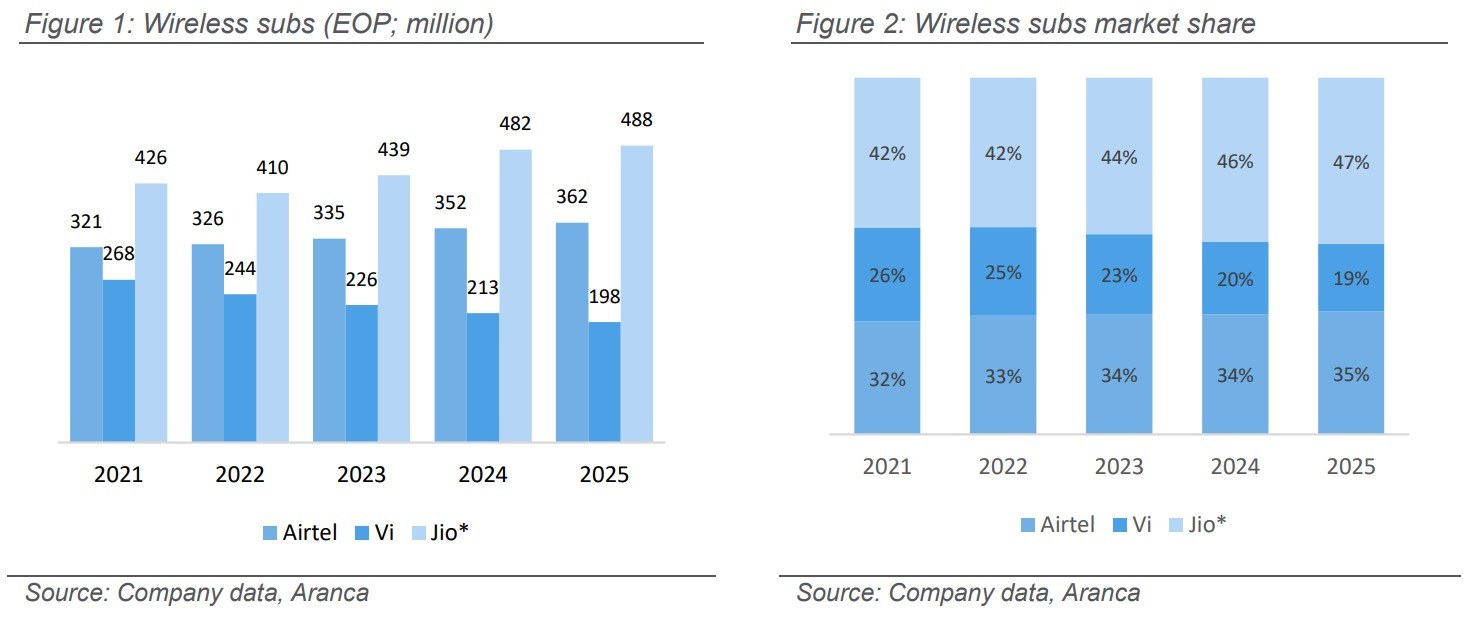

Wireless subscriber base

Vi’s wireless subscriber (EOP) market share has notably declined to 19% in FY25 from 26% in FY21. In terms of numbers, Vi’s subscriber base fell to 198mn in FY25 from 268mn in FY21. This substantial churn directly impacts its revenue, highlighting the acute need for effective customer retention and acquisition strategies. In contrast, Airtel expanded its base to 362mn in FY25 (35% market share) from 321mn in FY21 (32% market share), while Jio, the market leader, saw its base grow to 488mn (47% market share) from 426mn (42% market share) over the same period.

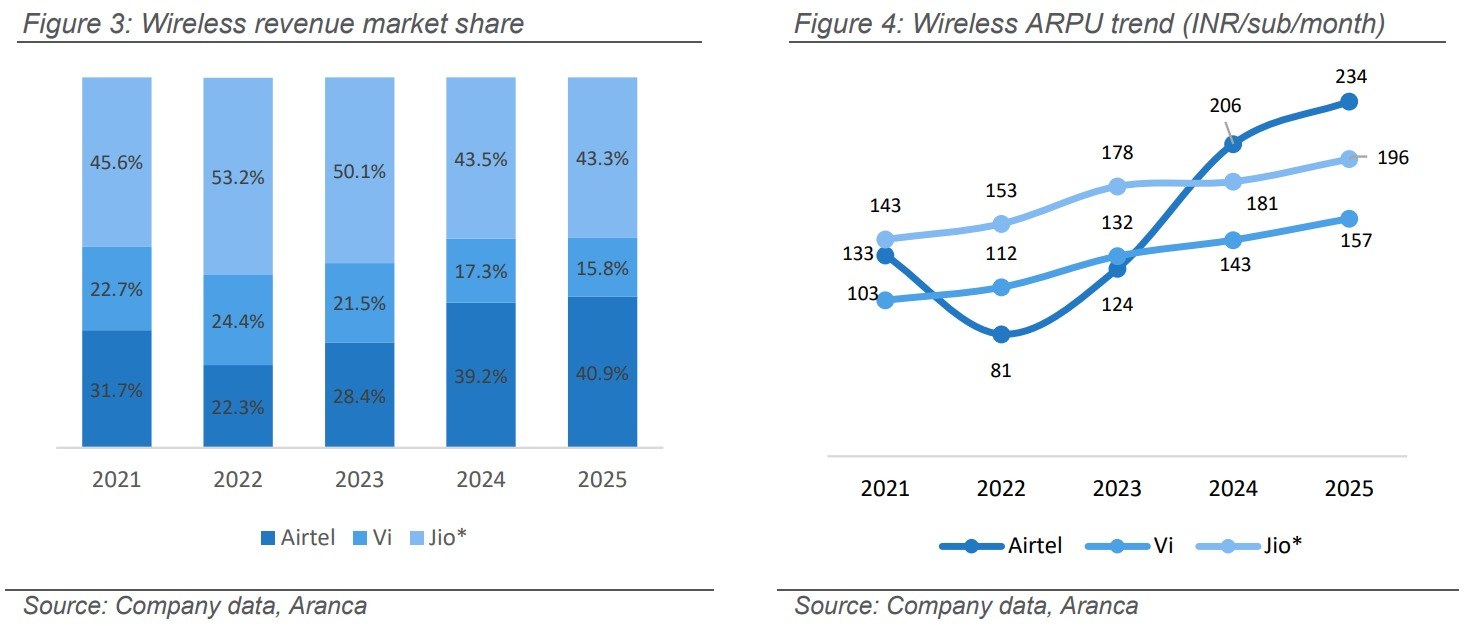

Wireless revenue market share

As of FY25, Vi's revenue market share stands at 15.8%, which is even lower than its subscriber market share. This disparity can be attributed to Vi’s relatively low average revenue per user (ARPU). While all three major telecom players have experienced ARPU growth over the past five years, Vi has struggled to narrow the gap with Airtel and Jio. The latter two have consistently invested in 5G technology and infrastructure upgrades, enabling stronger customer retention and allowing them to command a pricing premium over Vi.

AGR dues: The looming threat

What are AGR dues?

Adjusted gross revenue (AGR) is a metric used by India’s Department of Telecom (DoT) to calculate license fees and spectrum usage charges (SUC). A long-standing dispute between the operators and DoT is centred on what constitutes AGR—whether it should include only core telecom revenues or also non-core revenues. In 2019, the Supreme Court upheld DoT’s broader definition of AGR, including revenues from almost all sources, which was unfavorable for telecom operators. However, in 2021, the government introduced some reforms to ease the burden: i) AGR redefinition: Prospectively excluded non-telecom revenues; and ii) Dues moratorium: Allowed operators to defer AGR payments for four years. However, these changes applied only to future dues, leaving companies liable for past liabilities under the previous broader AGR definition. In 2025, the Supreme Court rejected telecom operators’ appeals to recalculate these dues, hence maintaining significant financial pressure on the sector.

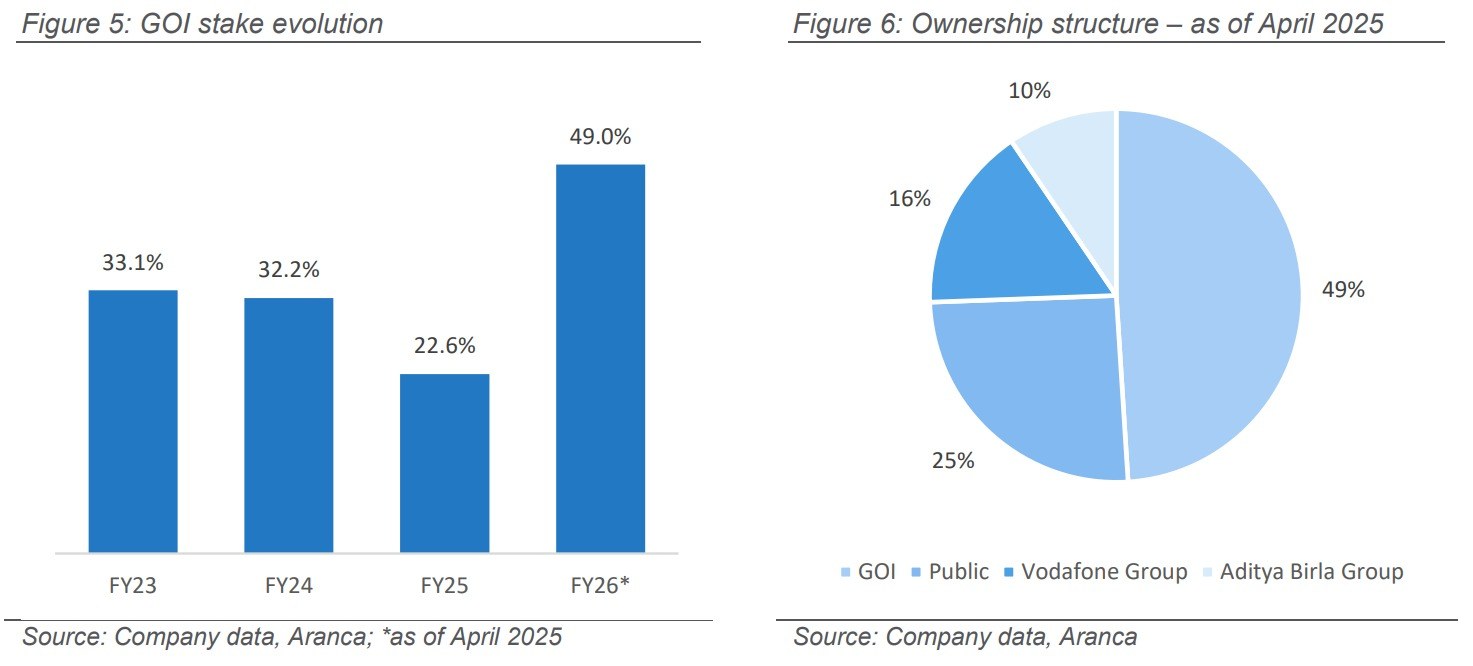

GOI stake and equity dilution

The Government of India (GOI) has implemented various measures over time to alleviate Vi’s financial distress. A key intervention involved converting VI’s dues into equity, providing essential funding support to the ailing telecom operator. GOI’s stake has fluctuated over the years: i) 33.1% at the end of FY23, ii) diluted to 22.6% by FY25, following VI’s INR180bn follow-on-public offering, a crucial fundraising effort aimed at addressing the financial challenges, and iii) sharply rose to ~49% by April 2025.

With the GOI holding ~49% stake, VI’s ability to raise capital through equity issuances is effectively constrained, significantly limiting its funding options. Consequently, the company is increasingly reliant on debt financing. Yet, securing new loans remains challenging, given the ongoing uncertainty surrounding its remaining AGR dues and its precarious financial health.

Capex deficit threatens long-term viability

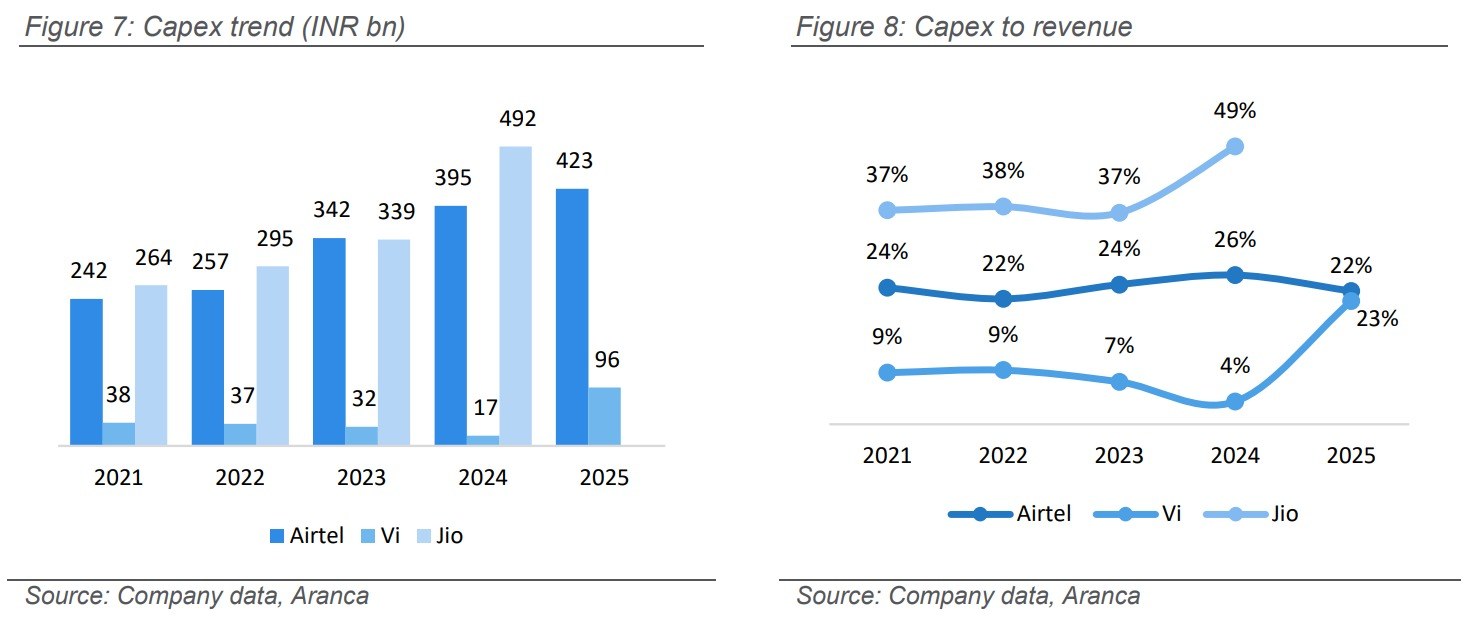

Vi has faced a critical capex deficit over the years due to its financial struggles. Vi’s capex significantly lags its key Indian telecom peers, Airtel and Reliance Jio Infocomm (RJIL). This underinvestment poses a substantial threat to its market share and subscriber base, as witnessed in recent years.

In FY24, Vi’s capex was ~INR17bn, starkly lower than Airtel’s ~INR395bn and RJIL’s ~INR492bn. Consequently, capex to revenue ratio stood at just 4% in FY24, compared with Airtel’s 26% and RJIL’s 49%. This disparity illustrates Vi’s persistent struggle to invest in critical infrastructure, directly contributing to its sustained loss of market share and subscribers.

Vi did see improvement in FY25, with total capex rising to ~INR96bn, boosting its capex to revenue ratio to 22%. This was primarily due to equity raise of ~INR260bn since March 2024 through promoters, FPO proceeds and key vendors. Vi has given a near-term capex guidance of ~INR50-60bn in 1HFY26, with key focus areas including: (i) raising 4G coverage, (ii) increasing 4G capacity, and (iii) further selective rollout of 5G services. However, the company’s long-term capex guidance of INR500-550bn over FY2025-27e remains highly uncertain without a clear and sustainable funding path.

Current state of Vi’s financial troubles

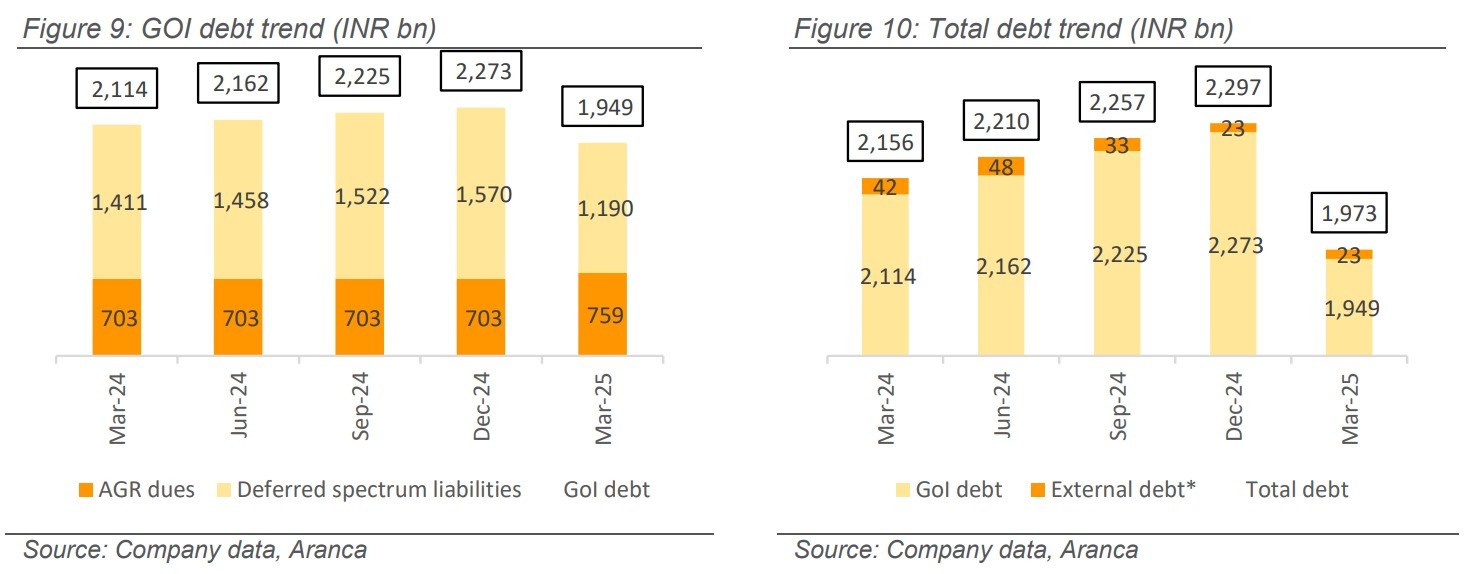

Telecom operators, including Vi, recently sought Supreme Court intervention for a waiver of AGR dues, a critical step toward reducing the financial stress on the industry. However, the Supreme Court refused to mediate between Vi and the GOI regarding the waiver, compounding the company’s financial distress. Meanwhile, the GOI maintains a firm stance on the outstanding dues, presenting a formidable financial challenge for Vi without this relief. The impact GOI’s dues has on Vi’s financials is substantial. As of March 2025, the AGR dues stand at ~INR760bn. Furthermore, the company’s deferred spectrum liabilities stand at ~INR1,190bn. This brings the total debt owed to the GOI to ~INR1,949bn as of March 2025.

The government has previously intervened to help Vi with its financial problems. In February’23, the government settled ~INR161bn of Vodafone Idea's dues into equity. This conversion included interest from the deferment of AGR and spectrum instalments. Vi’s net debt stands at INR1,873bn as of March 2025, with net debt (excl. leases) to an annualized EBITDA ratio at a towering 20x. Going forward, despite equity conversions by the GOI, Vi still has substantial debt repayments from 2026 and beyond. The debt repayments schedule stands at INR203bn in 2026, INR235bn in 2027, and INR331bn in 2028.

Aranca’s Takeaway

Vi finds itself in an increasingly precarious financial position, characterized by a debilitating debt burden and severe capex deficit. This chronic underinvestment over the years in its network infrastructure, particularly evident when compared with the substantial investments made by its peers, is directly translating into erosion of its market share and subscriber base.

Despite recent efforts (such as equity dilution, FPO, and vendor reliefs), the company is unable to stem subscriber churn and recapture revenue market share. The company's long-term financial improvement hinges on its ability to invest in its infrastructure through healthy capex, which would enable it to reduce market share losses and eventually increase its subscriber base. However, these capex plans can only be carried out with some financial relief from the GOI and debt financing from banks. The absence of a clear and sustainable funding pathway, along with the looming pressure of AGR dues, casts a significant shadow over Vi’s future.

In essence, Vi is caught in a vicious cycle: limited capex weakens its competitive position, leading to further market share losses, and strained financial performance, which, in turn, restricts capex even more. Without substantial and consistent financial support, coupled with a fundamental shift in its operational trajectory, Vi's ability to remain a viable third player in India’s highly competitive telecom market appears increasingly uncertain.

Siddhi Deo