The Looming Pension Fund Shortfall - Are Future Retirees at Risk?

Published on 04 Mar, 2020

The major shift in demographics with increasing life expectancy is expected to create problems for future retirees, who are expected to outlive their savings. In economies where the population is aging rapidly, one of the key challenges is to provide financial security for the older population. Most economies concentrate their pension fund assets in conventional investments markets – equities and bonds – thereby, depending largely on markets that are volatile and dynamic. This warrants a more cautious and planned approach by fund managers entailing diversification of pension funds from low-risk, low-return to high-risk, high-return asset classes. Moreover, at an individual level, a more prudent approach is required in terms of planning investments and increasing savings.

The global population is aging at an increasing pace. As per a United Nations report, the number of elderly is estimated to surpass that of children under 10 years old by 2030, and reach 2.1 billion by 2050. The incidence of aging is more pronounced in North America and Europe (more than 1 in 5 persons aged 60 or above in 2017). Aging in itself is accompanied with a lot of challenges; one of the main effects is on the financial security of the older population, so far ensured by company pension plans and government pension funds. Amid the growing population of retirees, pension plans are falling short.

Many companies are unable to handle their pension obligations, such as corporate giant General Electric (GE). The company was forced to offer pension buyout to former employees. The company also had to freeze the pension plans of over 20,000 salaried employees in the US. Conglomerates such as Federal Express, Verizon and General Motors were also compelled to take this harsh step. In a significant development, Dean Foods, the largest milk producer in the US, filed for bankruptcy in December 2019 due to high debt and increasing pension obligations. Shortly after, in January 2020, the second largest producer, Borden Dairy Co., filed for bankruptcy, citing inability to meet debt and pension obligations.

Government pension plans too are afflicted with a widening gap between assets and pension liabilities. National governments in most countries have schemes for their ageing population to provide them with an income in their golden years. However, these plans are largely skewed toward traditional assets that have a low-risk and low-return profile. As longevity increases amid improvements in healthcare and lifestyles, the drawdown period is becoming longer, requiring a larger pool of assets to provide from. On the other hand, as a larger portion of workforce enters the retirement age, their contributions to pension plans stop, while the drawdown starts.

Governments across nations are looking at various options to tackle this issue. For example, to reduce the pressure on pension plans, the Government of France proposed increasing the retirement age. However, this was not received well by its citizens, resulting in protests countrywide. Hence, governments need to tread carefully and judiciously weigh the likely reaction from the public.

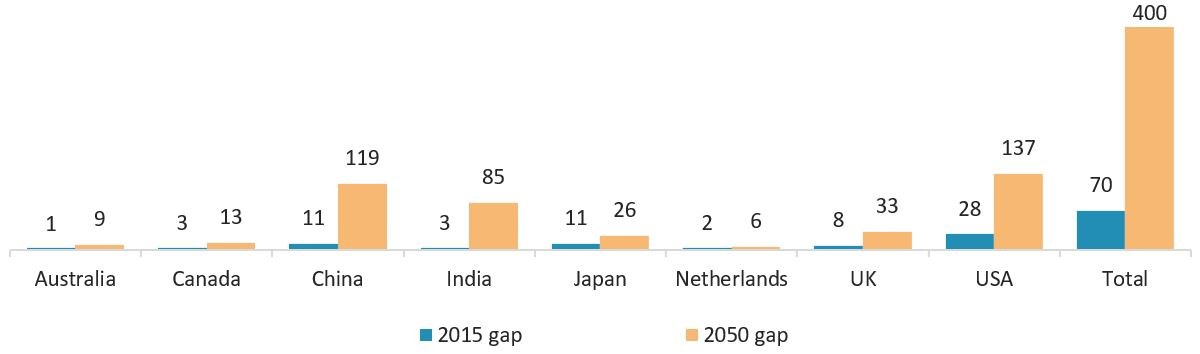

Government social welfare plans and company-defined benefit pension plans are under pressure globally. The countries listed below witnessed an overall retirement savings gap of US$70 trillion in 2015 (as per last available data). If corrective measures are not taken to increase savings, the gap is expected to widen to US$400 trillion by 2050.

Figure 1: Size of retirement savings gap (US$ trillions)

Source: Mercer Analysis for World Economic Forum

Pension systems world over are different. For example, in the US, the system comprises social security, employer-provided pension, and personal retirement savings. There are contribution plans such as 401(k), under which employees can choose their retirement investment. This plan does not have any maximum or minimum guarantee benefits.

One of the reasons for the current crisis is the lack of individual savings and investment and complete dependence on pension plans. There are other factors too. For example, in the US, four factors affect pension fund balances. First, many people in their 60s currently did not have access to 401(k) accounts at the start of their career. Therefore, their accumulation would be lesser compared to of a younger set of employees. Second, due to the lack of universal coverage, a worker may have been in previous jobs that did not have retirement plans. Third, since participants can access their account before retirement, at times accumulations leak out. Fourth, the fees charged depending on the size of the plan can significantly impact the net return on investments.

A few pension plans offered by countries are listed below.

Figure 2: Coverage offered by countries

Country |

Coverage offered comprises of |

|---|---|

|

Denmark |

A basic public pension scheme; an additional pension benefit scheme; defined contribution scheme (fully funded); and compulsory occupational schemes |

|

The Netherlands |

A public pension scheme (flat rate), and quasi-mandatory pension scheme (earnings-related); majority of employees are part of these occupational schemes which consist of defined benefit plans industry-wide and where earnings are based on average earnings over the lifetime |

|

The US |

A social security system based on earnings over the lifetime, together with a top-up benefit; and voluntary private pension plans (either occupational or personal) |

|

China |

An urban system and a rural social system characterized by pay-as-you-go pension plan, which includes employer contributions in a pooled account and employee contributions in funded individual accounts; and additional plans provided by some employers in urban areas |

|

Japan |

A flat-rate basic pension scheme; pension based on earnings; and voluntary pension plans that are supplementary in nature |

|

India |

An employee pension scheme (earnings-related); a defined contribution employee provident fund; additional pension schemes (managed by employers) which are majorly defined contribution plans; also, government schemes introduced as part of universal social security program |

Source: Melbourne Mercer Global Pension Index 2019

Is suppressing fixed income returns/yields worsening the pension shortfalls?

Traditional pension plans invest in bond markets, a relatively safe bet. With lower interest rates, yields on bonds decline, resulting in lower return on investment.

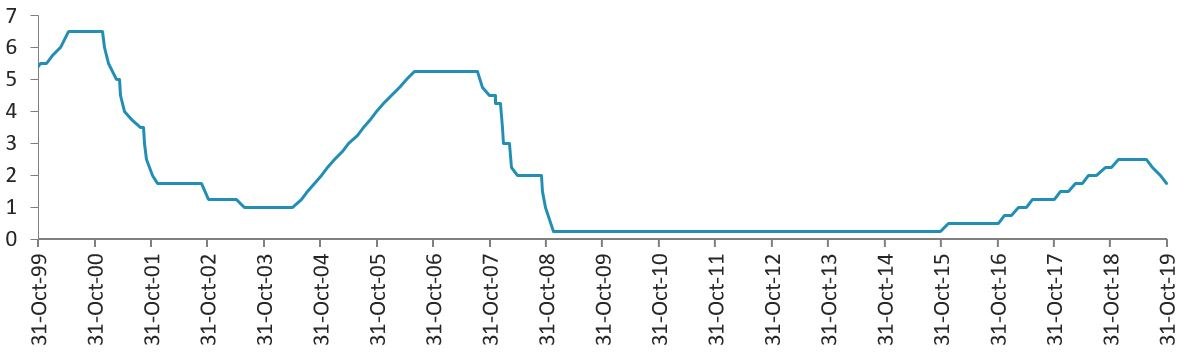

The US Federal Reserve hiked the interest rate in December 2015, after keeping it at near-zero levels for nearly a decade. The situation changed dramatically in 2018 when the interest rate was increased four times. In 2019, the Federal Reserve cut interest rates three times. After the rate cut in October 2019, the fed funds rate was in the range of 1.5–1.75%. This entire exercise in 2019 was to ensure that growth in the country continued, as 2020 is the crucial election year.

Figure 3: Fed interest rate cycle

Source: Reuters Eikon

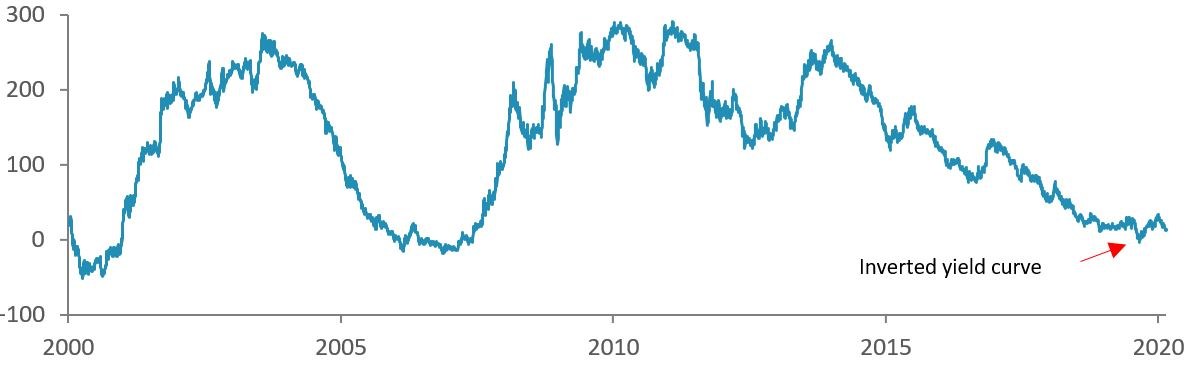

The yield curve, which is now un-inverted, had inverted in August 2019, implying short-term yields were higher than long-term yields. Consequently, markets became cautious as inversions have occurred prior to each recession in the US in the past 50 years. As pension funds tend to invest in low-risk, less dynamic, long-term instruments, an inverted yield curve and low interest rate do not bode well for fund managers.

Figure 4: Difference between 2-year and 10-year treasury yields (basis points)

Source: US Department of the Treasury

Importance of right mix of asset allocation

Fund managers need to tread more warily in terms of asset allocation, given the volatility in markets and everchanging economic conditions.

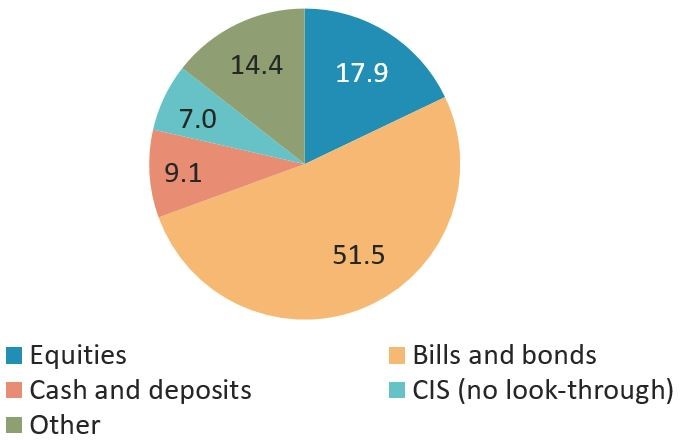

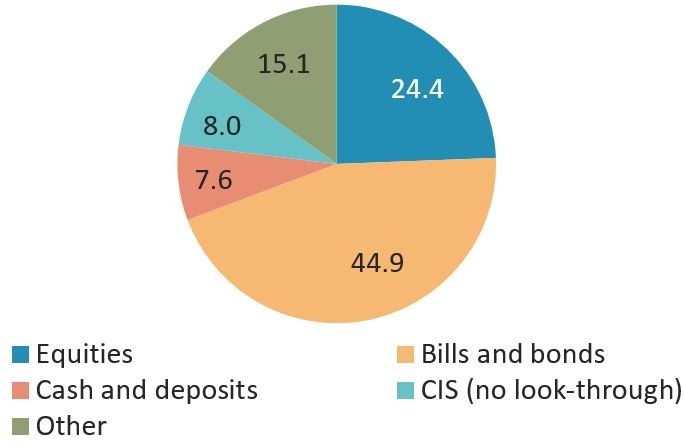

The proportion of equities in pension fund investments increased from 17.9% in 2008 to 24.4% in 2018, while that of bonds declined from 51.5% to 44.9%. Changes in asset mix are mainly due to a change in investment and asset allocation strategy. In 2018, almost 70% of pension fund assets were invested in equities, bonds and bills. Thus, any change in equity and bond markets can significantly affect the return on pension fund investments.

Figure 5: Asset allocation of pension funds in selected investment categories in 2008 and 2018

|

A. 2008 Over 29 reporting OECD jurisdictions  |

B. 2018 Over 36 reporting OECD jurisdictions  |

Source: OECD Global Pension Statistics October 2019

Suggestions to improve condition and conclusion

Market conditions are not always promising and, therefore, there is no guarantee of returns. This could create uncertainties for future retirees. However, a few steps can be taken to address the challenge.

At the investment level, fund managers must diversify the asset portfolio and take calibrated risk. This is needed to maximize returns on pension funds which are sinking fast. Although these investments usually have a low risk appetite, the need of the hour is to diversify and enter high-risk, high-return asset classes. Allocation of funds needs to change, and this calls for in-depth research on asset classes and scrutiny of the portfolio. Methods such as factor allocation and attribution analysis can be employed to scrutinize the portfolio and conduct thorough analysis.

At a personal level, individuals can increase their wealth through savings and prudent investment decision during their working years.

The issue needs to be tackled from multiple angles to ensure a secure future for retirees.

Esha Shah

Shreya Das