Surge in GCC sovereign bond issuances at attractive yields: Buyers underpricing risk?

Published on 22 Apr, 2020

Multibillion-dollar bond issuances in April 2020 by three Gulf Cooperation Council (GCC) countries – Qatar, Abu Dhabi and Saudi Arabia – have galvanized the fixed income market, especially the emerging economies segment. The attractive yields offered prompted fixed income investors to submit bids exceeding the issue size. However, the region is reeling under the impact of the slump in oil market, besides the economic fallout of COVID-19-induced lockdowns. Therefore, the question arises would the yields adequately compensate for the risks.

Qatar, Abu Dhabi and Saudi Arabia raising billions of dollars in sovereign debt

So far in April 2020, three Gulf Cooperation Council (GCC) members – Qatar, Abu Dhabi (part of the UAE) and Saudi Arabia – have raised or are in the process of raising around USD 25 bn of sovereign debt. First, Qatar launched a USD 10 bn Eurobond in three tranches of 5, 10 and 30 years that attracted USD 25 bn, or 2.5 times the issue size. Thereafter, Abu Dhabi launched a USD 7 bn bond, also in three tranches of 5, 10 and 30 years, attracting bids nearly 3.5 times the issue size. Recently, Saudi Arabia too launched an issue, worth USD 7–10 bn, in three tranches of 5.5 years, 10.5 years and 40 years, its first longest-tenure bond. Lured by the yields, fixed income investors are flocking to these issuances—the Saudi Arabian bond has attracted bids nearly 6 times the issue price, as per media reports.

Exhibit 1: Details of debt issuance by GCC countries in April 2020

Country | Issue Size (USD bn) | Tranches | Bids (USD bn) | Bid to issue (x) |

|---|---|---|---|---|

Qatar | 10 | Three tranches (5-year, 10-year, 30-year) | 25 | 2.5 |

Abu Dhabi | 7 | Three tranches (5-year, 10-year, 30-year) | 25 | 3.5 |

Saudi Arabia | 7 to 10 | Three tranches (5 and ½-year, 10 and ½-year, and 40-year) | 42 | 6 |

Source: Aranca Research

Spreads attracting fixed income investors

The spreads offered for these issuances range between 200 and 325 basis points (bps) over benchmark US treasury instruments of similar tenures; no doubt, they are highly attractive for fixed income investors. Central banks across the globe have cut rates, and central banks in major developed markets, such as the US Fed, have reduced rates to zero. Yield curves of major sovereigns are either close to zero or near negative for most part. As such, investors in sovereign bonds were faced with the challenge of finding the investment opportunities to deploy funds which would give them higher yields without compromising the portfolio’s risk profile. The investment grade sovereign credit issuances in these countries, with the stated spreads and yields, could not have come at a more opportune moment. For fixed income investors, the offers are ‘irresistible’, going by their comments in media. Moreover, rating agencies affirming the investment grade credit ratings for these countries has provided further reassurance in the face of the three main adversities: economic fallout of COVID-19 on the region, decline in oil market (compared to the start of the year) and uncertainty regarding demand.

Exhibit 2: Spreads and yields offered tenure-wise for each issuance

Country | Credit Rating (S&P) | Tranche | Yields |

|---|---|---|---|

Qatar | AA- | 5 year | 300bp over US 5 yr or 3.4% equivalent |

Abu Dhabi | AA | 5 year | 220bp over US 5 yr or 2.67% equivalent |

Saudi Arabia* | A- | 5 and ½ year | 315bp over US 5 yr or 3.49% equivalent |

Source: Aranca Research; Note: *- Issue still in market, final spreads and yields may change

Economic impact of COVID-19 in GCC region

The GCC region’s economy, like the rest of the global economy, is negatively affected by pandemic-related restrictions on movement and activities, ranging from partial curfews to 24-hour lockdowns. The region, home to millions of expats, is also witnessing a rise in cases among undocumented immigrants, who are reluctant to come forth for treatment, despite assurances from the government that they would not be required to disclose their identity. The epidemic has also reached the high corridors of power, with many members of the Saudi royal family being diagnosed with the infection. The more the virus spreads, greater the delay in easing restrictions and resumption of economic activities in the region. The IMF, in its latest economic outlook report published in April 2020, has slashed the 2020 GDP growth estimate for the Middle East region to -2.8% from +2.8% (previous update in January 2020). GDP of Saudi Arabia, the biggest economy in the region, is expected to contract 2.3% in 2020 vis-à-vis the earlier estimate of a marginal 0.3% contraction (as per previous update in January 2020).

Dependence on oil and volatility aggravating the situation

For the oil and gas producing countries in the GCC region, volatility in oil market is an additional concern, besides the negative economic impact of COVID-19-induced lockdowns. The region has historically been a major producer and exporter of oil and related products that contribute significantly to government revenues and have a strong bearing on its economic growth. The oil sector accounts for 30–50% of the GDP of major exporters, which indicates the close link between economic growth and developments in the oil market. Volatility in oil markets, therefore, does not bode well for these economies and would adversely affect exports, government revenues and fiscal balances.

Oil prices were under pressure in 2019 due to oversupply in the market amid slow growth globally. However, an agreement was reached between OPEC and select non-OPEC producers (such as Russia), together known as the OPEC+ group, to voluntarily implement production cuts of up to 2 million barrels of oil per day (roughly 2% of daily demand) in order to reduce supply and rebalance the market supported prices partly. However, in March 2020, the agreement fell apart as lead producers Saudi Arabia and Russia sparred publicly. With the deal ending, production increased immediately and producers offered price discounts in a race to gain market share. Consequently, oil prices nosedived, falling over 50% in March 2020.

As the decline in oil price would have severely affected the US shale oil industry (not party to the OPEC+ agreement), US President Trump took the lead in the effort to bring the OPEC+ group back to the negotiation table. In April, after marathon discussions, the group agreed to cut up to 10 million barrels of oil per day (or roughly 10% of production) among various producers from May 2020. However, the discussions were not smooth, as Mexico did not agree to its share of production cut, requiring another intervention from the US. Considering the level of commotion and lack of clarity regarding production cuts, the oil market is sanguine about actual implementation. Furthermore, the latest report from the International Energy Agency (IEA) states that demand for oil is expected to fall by 29 million barrels of oil per day in April 2020 (or roughly one-third of average demand in 2019). As such, the production cuts announced may not be enough to rebalance the market. Oil prices are reflecting the grim reality, by toppling again.

Exhibit 3: Brent crude prices (USD/barrel)

Source: Refinitiv

Bond markets looking to hedge against falling oil prices by way of higher CDS spreads

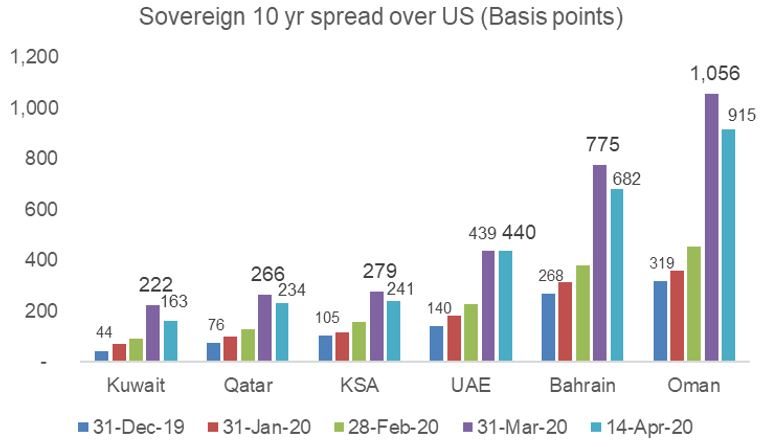

As economic growth prospects for GCC countries weaken, as COVID-19 spreads in the region and oil prices plunge, bond markets have reacted decisively, reflected in weakening yields on benchmark sovereign bonds as well as rise in credit default spreads (CDS), a proxy for cost of insurance against sovereign default. As the following exhibit depicts, CDS rose sharply by 200% to 400% for various GCC countries, and that too in a span of only 3 months, indicating the bond markets’ view of sharp rise in default risk for these sovereigns. In the first fortnight of April 2020, following the news of a new agreement to cut production by up to 10 million barrels per day of oil, CDS have narrowed but not substantially.

Exhibit 4: CDS spreads (over US 10-year yields) for GCC countries over time

Source: Aranca Research; Refinitiv; Note: UAE represented by Dubai

Yields offered on recent issuances compensating for growing risks?

Yields offered on recent issuances are undoubtedly quite attractive compared to prevailing yields for existing instruments. Comparing 10-year sovereign yields, Qatar’s new issuance yield of around 3.8% was higher than the then prevailing yield of around 3.6–3.7%. Abu Dhabi’s issuance yield, at around 3.2%, compares favorably to the prevailing 3% yield. Saudi Arabia’s new issuance initial yield of 3.9% would appear very attractive vis-à-vis the current 3.2% yield, and the final issue yield is expected to be tighter but above market yields. Moreover, Saudi Arabia has launched a 40-year bond, which is the longest tenure for any regional sovereign bond. The size of bids has been in multiples of the issue size, underscoring the attractiveness of issuances even during the current global turmoil. The market appears to have given a thumbs up, despite the risks, such as:

- Resurgence of COVID-19: Currently, capital markets are optimistic that the curve of infections would slope downward in developed economies, such as Europe and the US, which reported the highest casualties. Unprecedented measures such as extended shutdowns are now being replaced by plans to resume operations in phases in certain sectors of the economy. However, the evolving situation in countries such as China and South Korea suggests that we are yet to completely understand the nature of the virus. Asymptomatic transmissions are rising, in addition to new cases discovered following the resumption of international travel, which led China to seal its borders with Russia. The World Health Organization has also alerted governments against reopening economies before building adequate testing and healthcare capacity in place. If there is a resurgence in cases after the relaxation of shutdown, governments will be compelled to reimpose restrictions. If this happens, it will pave the way for ‘risk-on’ trades in capital markets that would lead to a decline in yields.

- Unprecedented uncertainty in oil market: Uncertainty surrounding demand for oil, crucial to GCC economies, is high (both immediate and long-term). The historical production cut of 10 million barrels per day (mbpd) agreed upon following intense negotiations is contingent on joint compliance by the parties to the deal. In the earlier round of cuts, Russia refrained from complying fully. This time, Mexico has raised objections, saying instead of complying with the 400,000-bpd production cut, it will restrict it to just 100,000 bpd. As per media reports, US President Trump has offered a solution wherein the US would reduce its production, absorbing Mexico’s share, for which the latter could ‘compensate’ later; however, the US cannot openly agree to cuts as this would be in violation of anti-trust regulations (instead, it believes market forces – demand and supply – would naturally lead the shale oil industry to reduce production). As such, the agreement appears to have been put together in a hurry, reflecting a desperation to indicate to the oil market that some action is being taken to address concerns. Besides, there is Saudi Arabia holding the Democles’ sword of offering price discounts in its bid to gain market share from Russia. Finally, demand may decline further as economic shutdowns dwarf the benefits of production cuts; this would mean fall in oil exports of GCC producers, in addition to the decline in oil price. In such a scenario, yields offered by issuers may not adequately offset risks.

Fixed income markets, keeping the dynamics in mind, have still voted in favor of issuers, going aggressively for bond issuances. Market participants may be taking comfort from the large forex reserves available with the issuers, relatively low debt-to-GDP ratios (compared to developed markets) as well as investment grade ratings affirmed by rating agencies recently. However, considering the unprecedented situation governments across the world are grappling with, the path to recovery is uncertain and with no precedent. Bond markets are quick in reacting to the spread of COVID-19 and expected impact on economies, evident from the rapid widening of CDS. Investors in recent issuances would do well to bear the risks in mind, especially if the rest of GCC countries, with weaker ratings, encouraged by the success of Qatar, Abu Dhabi and Saudi Arabia decide to follow suit.