Investment opportunities in distressed assets amidst Covid pandemic

Published on 16 Apr, 2020

In the wake of the COVID-19 pandemic, nations are deploying various measures to limit causalities. The crude price war between Russia and Saudi Arabia isn’t helping either. The negative impact of the outbreak is felt across sectors. The distressed debt industry will now go into an overdrive as businesses face shutdowns and unemployment rises. Which sectors get affected? How severe will be the impact? 2020 will be the crucial year…

Narratives are changing in less than a year

In September 2019, famous distressed debt investor and co-founder of Oaktree Capital Group Howard Marks said, “Investing in distress debt is a struggle today…. The economy is good, the capital markets are too generous. It is hard for a company to get into trouble”. His industry peers shared similar insights then. The Federal Reserve had lowered interest rates in its bid to offset adverse impact of the US-China trade war, equity markets had shrugged off a brief decline in August 2019, and yield pick-up on speculative grade corporate bonds had again slipped back to the lows seen after 2008. Distress was nowhere to be found.

Fast-forward to today and the entire narrative has changed

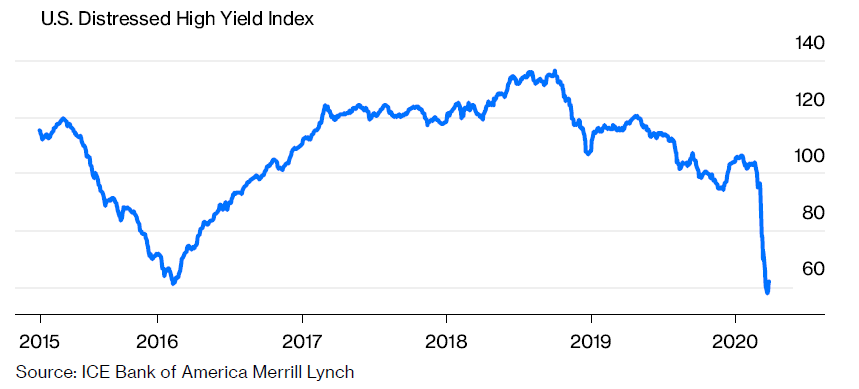

In just six months, Howard Marks is opining differently—he is pessimistic about the recovery of the US and global asset markets impacted by the pandemic. He predicts price markdowns, increased haircuts and a dearth of bailouts for some lenders. Junk bond spreads have more than tripled since September 2019 from 350bps to 1,100bps, with debt trading at distressed level reaching c. USD 1trn in the US alone. Price of distressed debt (bonds) has tumbled c. 40% in 2020 already.

Marks further compares the current crisis to the global financial crisis of 2008 and mentions that this time round, it would be highly unlikely that government bailouts would be made available to non-bank-lenders and funds that have supplied leveraged securitizations. Aggravating the situation, there is further concern over the sharp decline in oil prices and the ongoing price war involving Saudi Arabia and Russia, which is expected to impact the exploration industry’s capital investment cycle (particularly shale oil). Moreover, uncertainty pertaining to demand for crude (and in turn finished products) could increase as nations go into lockdown that could stretch for 3–6 months.

Where do we stand today and who has been impacted?

According to Pensions & Investments, by the end of March 2020, distressed debt in the US quadrupled in less than a week to c. USD 934m, reaching levels not seen since 2008. Junk bonds are yielding at least 10 percentage points above Treasury yield, while loans are trading less than 80 cents to a dollar. The total value is estimated to be higher as the calculation described above excludes medium-sized companies whose debt instruments rarely trade.

Distressed debt tied to the oil & gas sector exceeded USD 161bn (at the end of March 2020), up from USD 128bn a week earlier. Except utilities, most other sectors in the US, including transportation, retail, entertainment, telecommunications and healthcare, have reported higher distressed ratios (rising to double-triple digits). Distress in sectors such as automotive and auto ancillaries is even more severe, wherein investment grade companies are at risk as well. Ford Motors recently got downgraded to junk status.

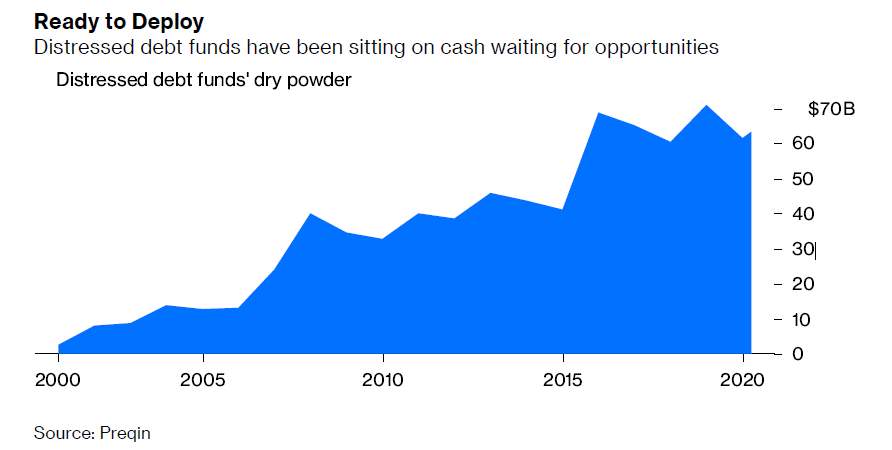

Consequently, new distressed funds are making headlines

According to Bloomberg, Highbridge Capital Management plans to launch two credit dislocation funds, worth USD 2.5bn in total; it is expected to complete fundraising in April 2020. Knighthead Capital Management requires additional cash totaling USD 450mn for its distressed debt fund. Silverback Asset Management is preparing to launch a USD 200mn credit fund; it aims to conclude fundraising by April 2020. Centrebridge Partners LP, in March 2020, activated c. USD 3bn of capital it raised in 2016, while Sixth Street Partners, plans to activate a USD 3.1bn contingency fund raised in 2018. Furthermore, Marathon asset management was able to draw USD 500mn into its opportunistic and distressed credit funds.

What do rating agencies anticipate?

Fitch recently published a report stating that anticipating price dislocation in high yield bond markets could lead to a surge in debt exchanges. The agency expects such transactions will be treated as restricted defaults. Fitch expects uncertainty in the economy and capital markets to continue in 2020 and anticipates that companies would experience some form of distress. Of these, issuers with unsustainable capital structure would have three options to restructure their obligations: file for bankruptcy or similar insolvency or intervention proceedings, opt for refinancing (typically arising when an issuer’s problem is due to liquidity rather than solvency), or resort to Distressed Debt Exchange (DDE).

Outcome

While debt markets (bond and loan prices) have already taken a hit due to the outbreak of COVID-19 and low crude price environment, actual defaults are yet to happen. Corporates will experience deteriorating liquidity conditions to begin with, that would lead to lower headroom to take additional debt and eventually worsen solvency and, in the interim, result in a rating downgrade by a couple of notches. Corporates with single B ratings are most likely to experience the highest probability of default. Sectors with the highest levels of stress would be airlines, aircraft lessors, hospitality, entertainment, energy, automotive.

Conclusion

Until the virus is eradicated or vaccine gets developed for Covid-19, the lockdowns, partial or complete, will continue, negatively impacting markets and industries. The debt market is no exception to the trend and will have to go through the grind. Even after the recession or economic downturn is over, it is highly unlikely that things will go back to as they were before. The only way for companies to survive and thrive will be to adjust to the new environment. As default levels rise, the situations will result in opportunities for distressed debt investors.