Growing Competition in US Media Industry Driving Acquisitions

Published on 17 Feb, 2020

The astronomical success of Netflix has disrupted the traditional entertainment market, luring tech players to the newly created SVOD segment and forcing incumbents to adapt. With content as the key differentiator, companies are either investing heavily in original content or acquiring traditional companies with popular existing content. Some companies are also using this opportunity to diversify or enter new segments through acquisitions. The past year has seen many major deals, including mega mergers such as Disney-Fox Corp and AT&T-Warner. The momentum is expected to continue as small media companies look to partnerships to boost scale or gain synergy.

The US media and entertainment (M&E) industry, which includes movie studios, cable, satellite and other modes of entertainment, is the largest in the world, with a strong following globally. Worth $717 billion as of 2017, it is estimated to grow at a 2.4% CAGR to $825 billion by 2023 Competition in the media landscape is intense due to technological improvements, increasing internet speed and rising internet penetration driving demand for video content. With content increasingly being delivered over the Internet, companies are no longer required to invest in proprietary infrastructure (such as cable network or satellites) to reach customers. This has enabled startups and tech companies with deep pockets to enter the space and seek a share in the growing Subscriber Video on Demand (SVOD) market. The traditional business model of ad supported entertainment is declining rapidly; this is reflected in the 2.2% fall in TV ad spending in 2019, compelling companies to look for new revenue streams. The fast changing scenario has created a fertile ground for mergers as companies try to adapt to the new digital business model.

Factors Leading to Consolidation

Streaming effect

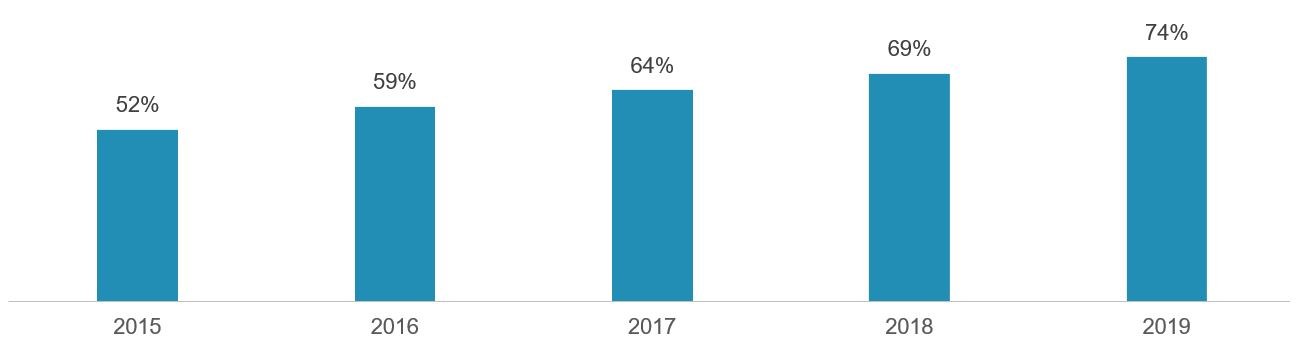

Subscriber video on demand has taken consumers by storm─74% of households in the US currently have an SVOD service, while its subscriber base surpassed the cable subscriber base for the first time in 2017. SVOD is cheaper than cable network and major providers are investing heavily in content; this is encouraging consumers to cut the cord with other modes.

Figure 1 SVOD Penetration in US Households (% of Households with SVOD)

Source: Marketingcharts

The success of SVOD has piqued the interest of both traditional media companies, such as Disney, as well as non-media companies like telecom and tech players. For non-media companies, SVOD can serve as a differentiator, a means of acquiring and retaining customers. It can also help in creating an ecosystem of products/services, wherein SVOD services could be bundled with device offerings. Amazon and Apple are specifically using SVOD as a means of creating an additional subscriber revenue stream and to lure customers. Two years after completing its acquisition of Warner, AT&T is now planning to launch wireless packs with HBO Max bundles to drive subscriptions; this is similar to what its rivals Verizon and Comcast are doing with Disney+ and Netflix, respectively.

Content is King

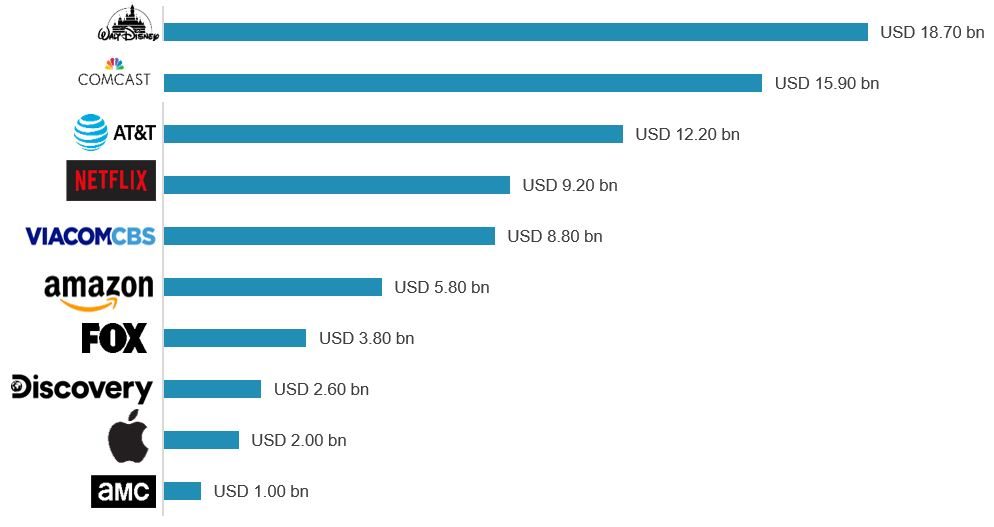

An SVOD service provider needs to have a quality catalogue of content to attract as well as retain customers. While the traditional cable business allowed content creators to both host and license their content to other broadcasters, SVOD as a differentiation necessitates that creators hoard both their IP and content. Netflix learned this the hard way when Disney pulled out the Marvel IP from their platform. The battle for content has resulted in companies pledging huge amounts of money for both quality and original content.

Figure 2 Estimated Non-Sports Video Programming Expense of Select Companies in 2019

Source: Moffett Nathanson, Company Reports

Many of Disney’s recent mergers were guided by the need to create a catalogue of popular content for their Disney+ service. One of the rationales behind the Viacom-CBS merger was to create a company with a strong content portfolio and capable of competing with the likes of Netflix and Disney.

Transforming Businesses by Building Scale and Diversifying

Acquisitions enable companies to explore new revenue streams or synergies by entering new segments. With the lowering of entry cost and amid growing competition in the industry, media companies need to build enough scale so as to be able to undertake the desired expenditure on content, besides directly interacting with the customer.

Disney’s acquisition of Fox not only gave it a powerful catalogue of content but also facilitated its transformation into an end-to-end media behemoth. Disney had multiple high-quality studios to produce content as well as channels and streaming services to distribute to consumers. This size alone gives it enormous bargaining power over media stakeholders from cinema owners to advertisers. By acquiring Fox, Disney also gained control over Hulu, which it is bundling with Disney+ to attract more customers.

Viacom and CBS are joining hands to gain the requisite scale for investing in streaming assets and competing in a highly crowded market. However, unlike Disney, instead of keeping their content exclusive, the merged entity is planning to license its content to other streaming services as an additional source of revenue. This is a bold move since allowing other SVOD services to host their content could dent their own service’s value proposition as well as subscriber base.

For telecom companies like AT&T, acquisition of media companies provides access to content, besides building synergies in the form of wireless plans bundled with video subscription. The repeal of net neutrality will also allow telecom companies to favor their own services through higher data caps and bandwidths, compared to rival services. The ability to control internet backbone will give telecom companies negotiating power during licensing agreements

Deals Galore

The year 2017 was a landmark for the M&E industry ─ a high number of deals were signed, including major ones such as Disney-Fox Corp which significantly impacted the industry. 2019 ended on a marginally higher note compared to 2018 and includes two significant deals, Viacom-CBS and SBG-Fox Networks deal.

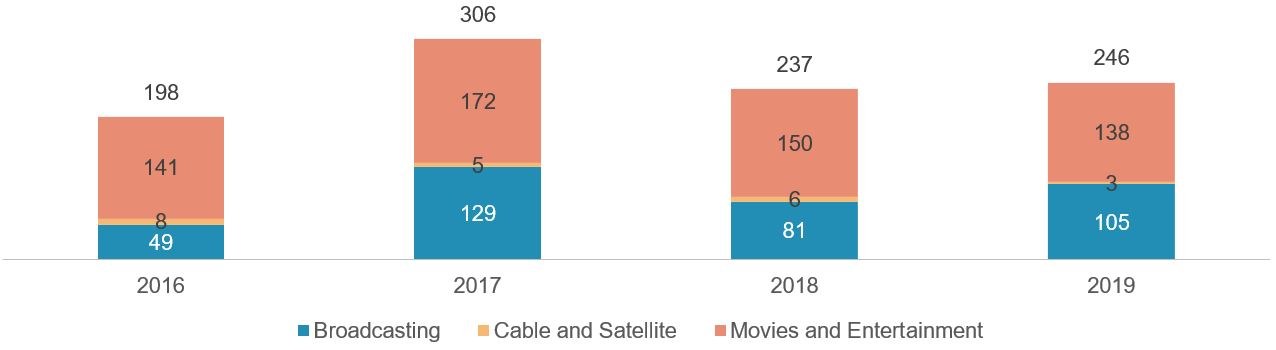

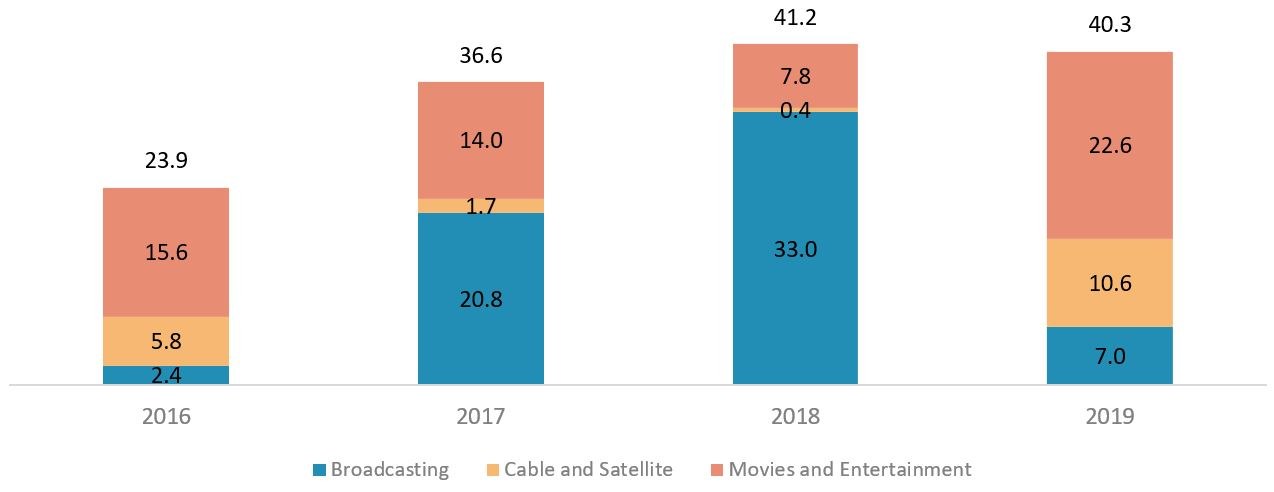

Most acquisitions have been in the movie and entertainment segment, followed by broadcasting. Cable and satellite is a mature industry and highly concentrated with a few players such as AT&T, DirectTV and Comcast dominating the market; this explains the lack of transactions in this segment.

Figure 3 Transactions in US Media and Entertainment Industry

Source: S&P Capital IQ

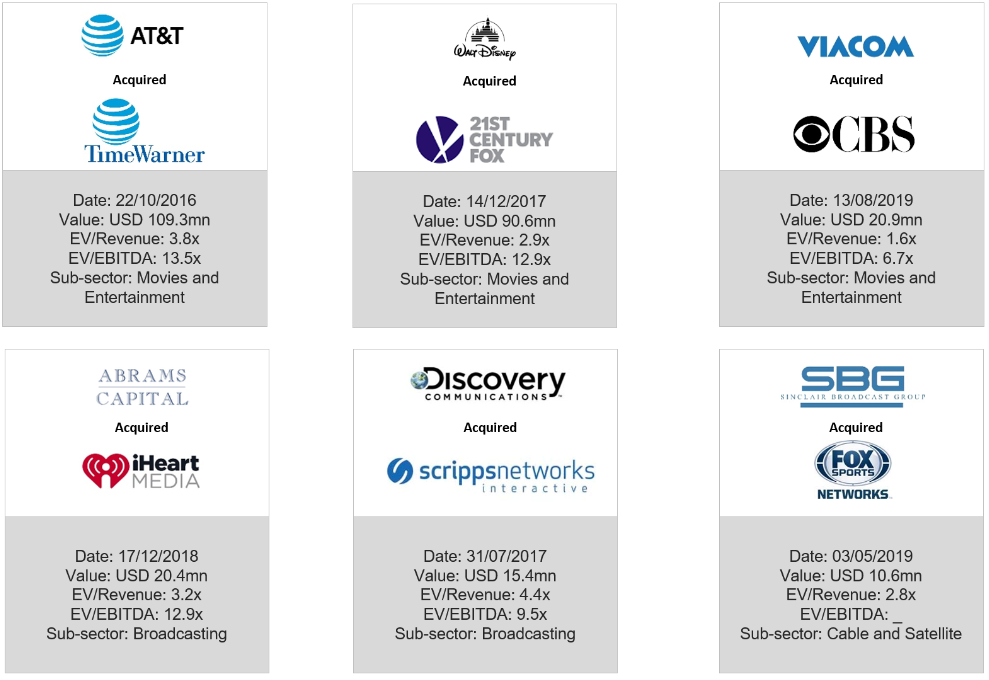

Movies and broadcasting dominated the M&A space with blockbuster deals – AT&T acquired Warner, while Disney acquired Fox Corp. Disney-Fox Corp is the biggest transaction over the last few years, 4x larger in size than the next biggest transaction which is the Viacom-CBS deal. The Sinclair deal was the only notable one in the cable and satellite segment.

Figure 4 Major Transactions in Industry

Source: S&P Capital IQ

Figure 5 Total Transaction Value in US Media and Entertainment Industry (USD bn)

Source: S&P Capital IQ

Note: Excludes Disney-Fox and AT&T-Warner due to size of these transactions

Transaction value grew 53% between 2016 and 2017 but has been more or less steady over the past few years. Deal activity was strong in broadcasting in 2017 and 2018, but slowed in 2019, picking up instead in the movies and entertainment segment.

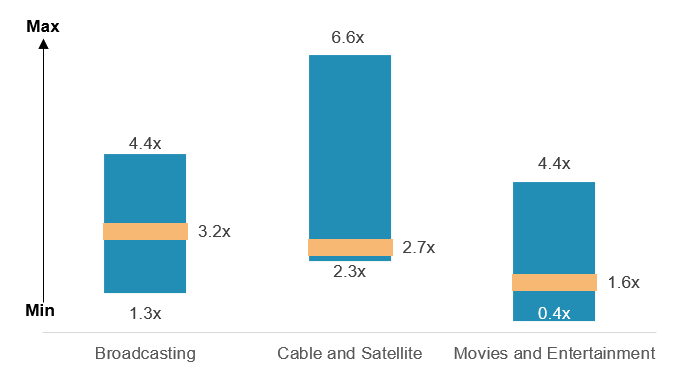

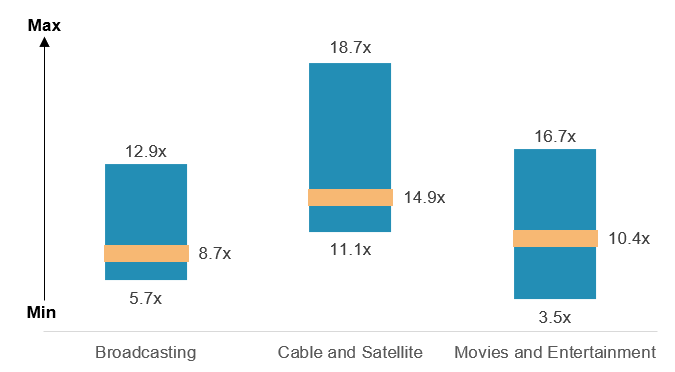

Figure 6 Transaction Multiples

|

EV/Revenue  Source: S&P Capital IQ |

EV/EBITDA  |

The spread of EV/Revenue multiple across segments deals was in the range of 3–4x. Cable and satellite deals were completed at higher multiples than those in other industries.

Even in terms of EV/EBITDA, the movies and entertainment segment had a much higher spread than broadcasting and cable and satellite. Overall, cable and satellite deals were at a higher premium.

The AT&T-Warner and Disney-Fox transactions, the biggest in the industry, took place at a EV/Revenue multiple of 3.8x and 2.9x multiple, respectively, a premium of almost 100% over the median multiple. The EV/EBITDA multiples were 13.5x and 12.9x respectively and were more in line with the median multiple.

The Future

While each media company is planning to launch an SVOD service, the market is already saturated with services. Newcomers will need to invest heavily in marketing and content in order to attract subscribers and in technology to deliver content. Licensing of content used to be a key part of the business model adopted by studios, but with the licensing model not as profitable as SVOD, content creators are preferring to hold on to their content to provide it as their own service.

The media M&A space has been very active in the past with both blockbuster and minor deals ─ this is likely to continue in future. The new age business model entails high capital expenditure and global distribution which will necessitate consolidation. In the new media landscape, any company with enterprise value less than $50 billion is at a severe disadvantage and must either consolidate or sell out. This is great news for studios like MGM and Sony that have recognizable content and can inflate the value of their catalogue as part of acquisition talks.

While the pace of deals is expected to continue, the momentum would not come from major companies. After a string of high-profile acquisitions, Disney has announced plans to slow down. Netflix has always been cautious about acquisitions, preferring to leverage its significant trove of data to invest in originals, and we believe the trend would continue. After the launch of Apple+, Apple may be looking to acquire a production studio in order to boost the content currently available on the service. While ViacomCBS is just coming out of a major merger, it would still need to consider another merger in order to compete with the majors. Smaller companies such as Discovery, AMC Networks, Lions Gate, MGM and Sony are expected to participate more actively in deals.