Existential Risk Management – Managing the Risk of Extinction

Published on 22 Jul, 2020

The global pandemic has once again bought fore the need to have risk management and business continuity plans to deal with crises. As COVID – 19 spread across the world, it spelled doom for the global economy and many companies were forced to declare bankruptcy. Could this have been avoided if there was a blueprint for disaster management, readying them to face unprecedented challenges?

Global catastrophes - from the various pandemics, sovereign defaults, liquidity crises, wide fluctuations in macro variables to a host of other unprecedented events - have exposed how fragile modern financial systems are. More recently, coronavirus has spelled death sentence for many big and small enterprises throughout the world. Businesses like airlines, tourism, hospitality, and retail are facing existential threats while other industries are facing severe challenges, some more fatal than others.

Businesses have traditionally focused predominantly on business and associated risks. The 2007 Financial Crisis and the destruction that ensued started the conversation on managing the risks of existence and many companies formulated or strengthened their crisis management and business resumption plans. Many eventualities, such as reputational, legal, and other remote risks that were hitherto ignored and deemed too remote to consider and now receiving the attention they deserve. Recent developments in the world, from civil unrest in the United States to tensions brewing between India and China, have demonstrated the importance of preparing proactively for catastrophes that seem implausible but are probable. The chart below demonstrates spike in establishment deaths during the financial crisis of 2007-08.

Quarterly establishment births and deaths, 1993-2015

Source – US Bureau of Labour Statistics

Any company which wants to safeguard its existence should establish a crisis management and business continuity function. The size of the function will depend on the scale of operations of the company. The exercise of existential risk management will involve rigorous scenario and sensitivity analysis, utilizing the advancements in data analytics and artificial intelligence (AI) as well as expert suggestions to simulate stressed circumstances. One example of a coordinated response is set out in an April 2020 report published by Accenture titled ‘Continuity in Crisis - How to run effective business services during the COVID-19 pandemic.’ The report outlines teams that helped Accenture in keeping afloat its business. Some of these teams were – Lead response team, Work from home enablement team, Robust communication team, Customer engagement team and Command centre team. Building a human + machine workforce, employing agile and elastic workplace models and establishing a resilient culture are some of the ways mentioned to build a sturdy organisation.

Best practices for existential risk management are:

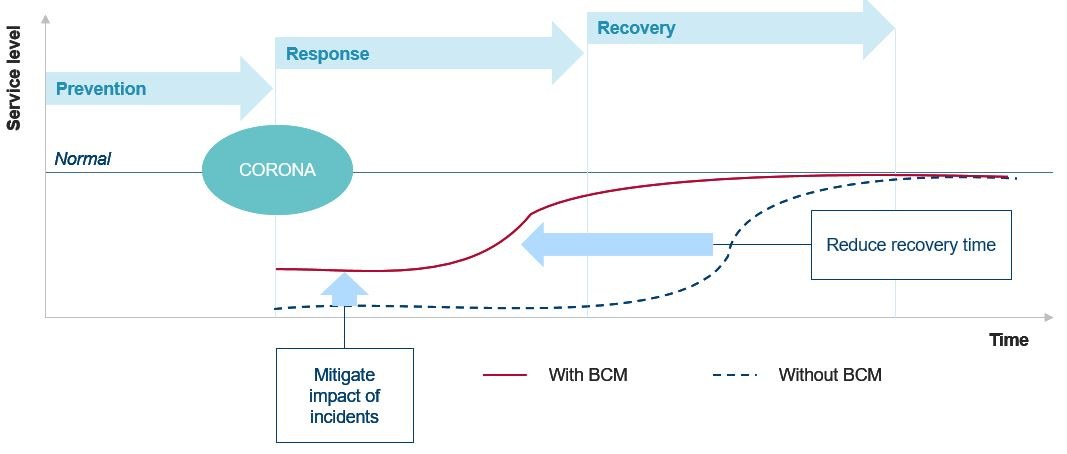

Designing Crisis/Incident Management, Business Continuity, Business Resumption and Disaster Recovery plans - These plans should define the when, who, where and how a co-ordinated response will be initiated in the event of crisis. The plans must be dynamic, evolving constantly to adapt to changing environment. They must be regularly tested for effectiveness and communicated across the value chain to ensure that employees are well aware of their roles and responsibilities in case of any eventualities. Institution of robust Business Continuity Management (BCM) will ensure that the organisation recovers significantly quickly during unforeseen events, as is shown below.

(Source – Risk Management and Internal Audit in time of Covid-19 - KPMG)

- Separate plans of action must be in place for different crises, as each will have a different impact on the business. Some examples of factors that can affect dissolution (challenge the going concern of an entity) and a list of catastrophes to consider are –

- Infectious disease outbreak.

- Breakdown of IT Infra, cyber-security attacks, data fraud.

- Political instability, social risks such as humanitarian crisis, social unrests, popular movements, riots, terrorism etc.

- Natural disasters.

- Pivotal change in government policies regarding matters fundamental to the business.

- War and subsequent embargo with countries forming a part of the supply chain. This would also involve consideration of disruption of global value chains and barriers to cross border movement of people and goods.

- Reputational risk, bad press, loss of confidence brought on by fraud and other moral and ethical fallouts.

- Regulatory, legal or contractual breach.

- Abrupt obsolescence of product/technology on which the entity predominantly depends.

- Prolongation of recession occasioned by other calamities.

- Extreme movements in business and macro variables.

- Extreme and sudden movement in demographics.

For each of these scenarios there must be a separate detailed plan. Plans must Identify factors that are most likely to prove detrimental to the survival of the organisation in periods of acute stress. The crisis management plan should also chalk out separate course of actions for different durations and intensities of crises.

- Some of the tools for managing existential risks are:

- Rigorous cash flow forecasting incorporating all plausible scenarios. Latest developments in AI and machine learning have enabled development of prediction models which are of great utility. Services of experts can also be availed to simulate scenarios. To ensure its robustness and usefulness, the scenario analysis must be sufficiently extensive with many nodes of possibilities at each step.

- Stress testing business and macro variables, like sales, demand, price, raw material availability, tax rates, interest rates and carrying out sensitivity analysis on solvency and liquidity ratios, capital and other metrics detrimental to the survival of the business.

- In addition to preparing internally for contingencies, external risk management tools must also be utilised, like – insurance, special situation bonds like catastrophe bonds and other specialised hedging tools like weather derivatives etc.

- Plans for managing fixed costs during periods of shutdowns must be thought-out. Cash optimization to identify opportunities to decelerate burn rate and preserve liquidity should be planned. The aim is to hibernate and survive in a state of suspended animation by rationalising contractual cash outflows.

- Working capital analysis to assess options to accelerate collections and use liabilities as a source of funding in times of stress.

- The aim must also be to quantify impacts and losses to better understand the severity of and facilitate comparison among different scenarios.

- COVID-19 has exposed the vulnerabilities of quantitative financial models (for example, expected loss provisioning, capital adequacy and risk weighted assets calculation etc.) There are several reasons for this – first, model assumptions were developed in pre-COVID era and second, the inadequacy of using historical simulation as a means for estimating future. This necessitates having models specially designed to be of use in times of extraordinary and unprecedented situations with parameters calibrated accordingly.

- Equally important is the recovery plan and it must be as comprehensive as time and other resources permit. The business resumption phase of the plan must consider various alternate realities of recovery and simulate the recovery. Expected support/relief measures by the government can also be incorporated if they are likely.

- Another layer of preparation in the form of correlation analysis could be used to consider the cascading effect of these scenarios happening simultaneously. This will render complex scenarios comparable. Interdependencies between risks and functions must be studied in some detail to anticipate the speed and extent of inter-functional diffusion and spill-over of risks.

- An evaluation of crisis management and business continuity plans of third-parties which are important for the existence of our business must also be carried out.

- A trade-off must be struck between costs and benefits of existential risk management. Plans must be scaled depending on the size of the businesses.

- The financial crisis of 2007-2008 has brought forward a host of other risks that were erstwhile ignored, namely – counterparty risk, wrong-way risks etc. In a crisis situation, when the stress is pervasive through the entire system, it is especially important to consider these risks.

Some of the points mentioned here come under purview of other risks also. The existential risk management is aimed to study, anticipate and safeguard against those events (irrespective of the type of events) that are so severe so as to prove fatal to the going concern/continuity of business.

It must be understood that an exercise like this cannot be exhaustive and can in no way completely hedge the business from all the unforeseen circumstances. Yet, we cannot give in to the vagaries and uncertainties of time and do our part in planning to secure the survival of our business during times of great turmoil.