COVID-19: Impact on US M&A Market

Published on 23 Apr, 2020

The ongoing health crisis, coupled with the resultant economic slowdown, has severely impacted the US M&A market. Numerous deals were either put on hold or cancelled in the last one month. Though in the medium term the recovery of the market would be sluggish, going by past economic downturns, this could be the right time to sign M&A deals. During downturns, quality companies are available at 13–21% valuation multiple discount, while previous cases show that deals carried out during this period generated almost 10% higher returns for shareholders.

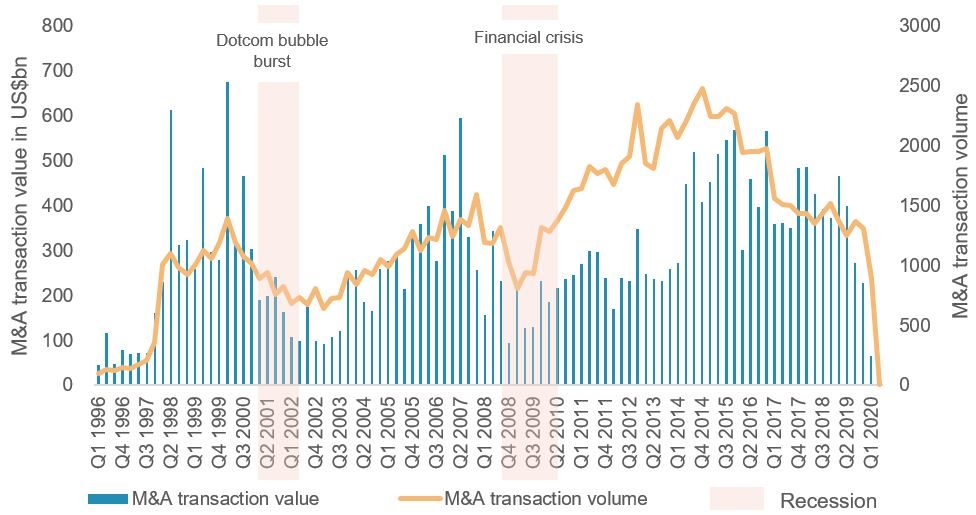

M&A activity directly correlated to economic growth and decline

Outlook for the US M&A market for 2020 was positive, with both M&A and capital raising activities expected to increase. However, the coronavirus outbreak, followed by the economic downturn, has put a brake on M&A activity in the US—transaction volumes in 1Q plunged 32% over the last quarter and 35% compared to the previous year.

Amid the current turmoil, while companies are focusing, on the one hand, on tackling the global health emergency, they are also working on plans regarding how to proceed once the COVID-19 crisis is over. According to a recent KPMG survey of ~2,900 C-suite executives globally, ~56% intend to scout for inorganic growth opportunities over the next 12 months.

US M&A cycles and economic recessions

Source: S&P Capital IQ, Aranca Research; Note: As of 13 April 2020

Channel checks conducted by Aranca suggest the US M&A market would be bearish in the near term, given the significant surge in COVID-19 cases. Nonetheless, once the pandemic is contained and the situation normalizes, M&A activity would pick up in the medium to long term, considering the anticipated pent-up demand in the second part of the year. However, the market is also treading cautiously, fearing the health crisis may worsen; if this happens, the volume of activity could decrease across the board.

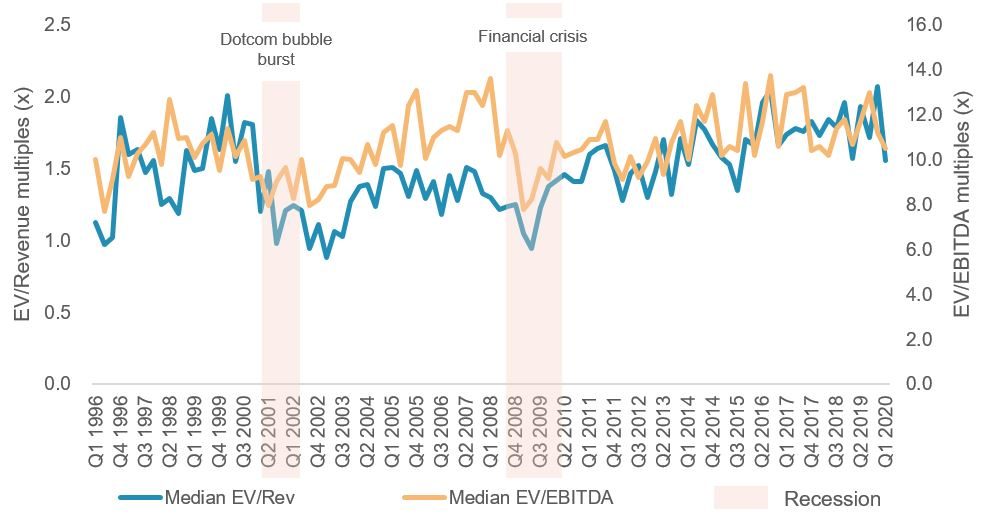

Median M&A valuation multiples tend to fall during downturns

Over the last couple of decades, M&A valuation multiples have generally increased, but median multiples have declined significantly during downturns. During the 2008 financial crisis, the median ratio of M&A deal value to revenue declined 13% on average, while the ratio of M&A deal value to EBITDA fell 21% compared to previous years. The decline in M&A multiples during this period provided an attractive opportunity to acquire high quality assets at subdued valuations that would drive growth amid recovery in market.

US M&A valuation multiples and economic recessions

Source: S&P Capital IQ, Aranca Research; Note: As of 13 April 2020

We believe as COVID-19 spreads and the economic slowdown continues globally, top companies across sectors may face financial difficulties and M&A valuation multiples will decline sharply. This would provide an attractive acquisition opportunity for companies that have built a healthy balance sheet (leveraging the previous economic boom) and created long-term value.

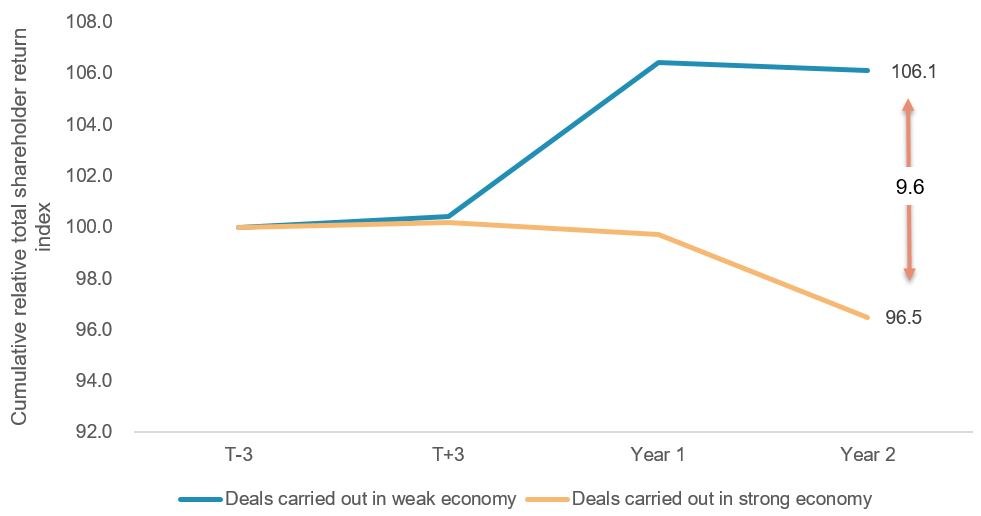

M&A deals carried out during downturns generate higher returns for shareholders

As seen so far, M&A deals signed during economic slowdowns have fared better than those entered into during stable growth phase. An analysis by BCG reveals that companies that made acquisitions during downturns generated 9.6% incremental returns for shareholders vis-à-vis deals executed when the economy was stronger.

Acquisitions made during the downturn fare better in the long term

Source: BCG Analysis

The incremental outperformance of these companies is attributed to acquiring quality business at lower valuation multiples and positioning the business better amid economic recovery. We believe investors that are ready to take the risk will fare better once recovery sets in the long term.