Key Trends in Private Equity Fundraising for 2025

Published on 12 Aug, 2025

Private equity fundraising remains a key indicator of investor confidence and market direction, reflecting shifts in capital deployment and strategic priorities. As market dynamics evolve, changes in fundraising activity signal adjustments in investor risk appetite and focus. This edition of the PE Fundraising Report analyzes H1 2025 trends in deal activity, fund sizes, regional focus, and fund types. It also highlights top-performing PE funds and provides a forward-looking industry outlook.

Summary

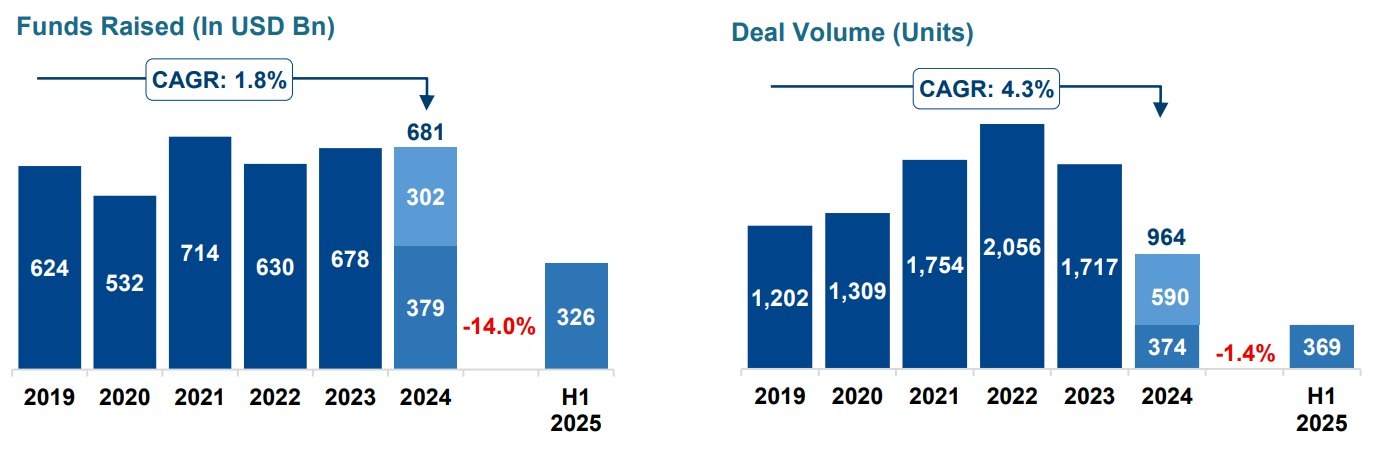

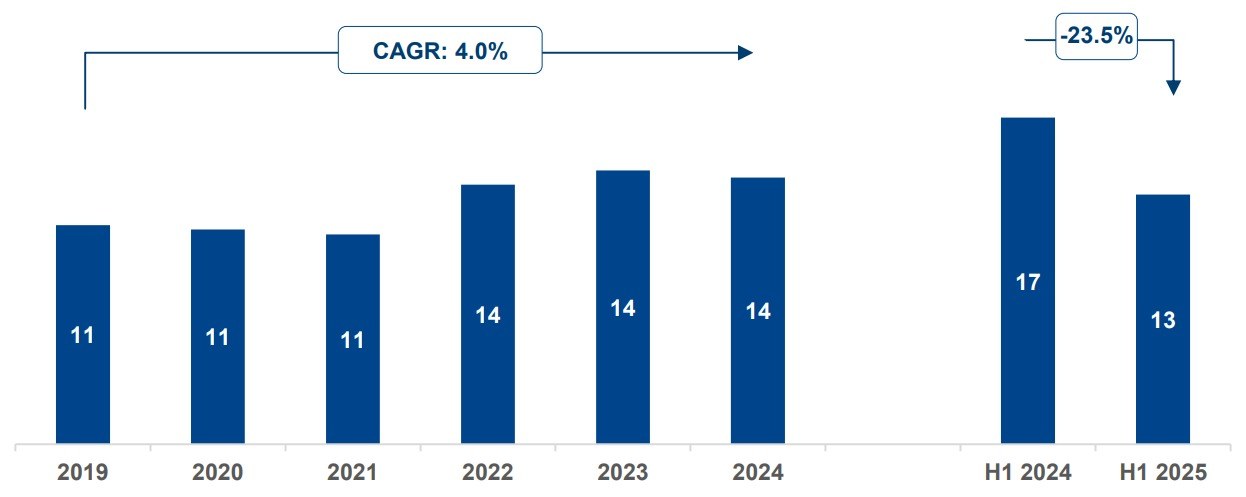

- Decline in Fundraising: Funds raised by PE firms totaled USD 326 Bn across 369 deals in H1 2025, marking a 14.0% decline in value and a 1.4% drop in volume compared to H1 2024. Rising macroeconomic pressures, including elevated interest rates, persistent inflation, and LPs’ (limited partners) reduced capital payouts amid a weak exit environment, drove the slowdown.

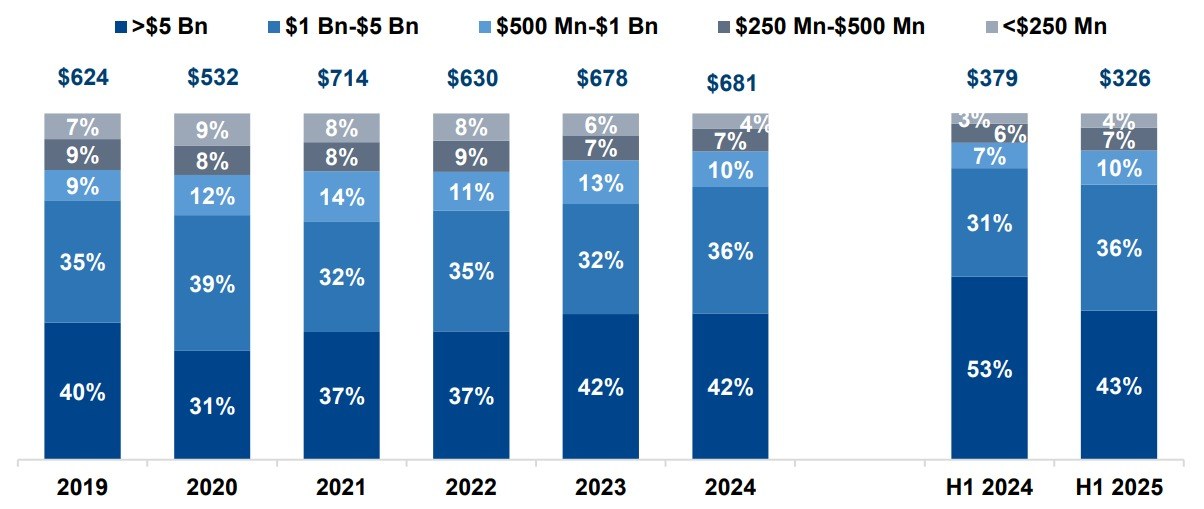

- Small and Mid-Sized Fund Preference: Small (under USD 500 Mn) and mid-sized (USD 0.5–1 Bn) funds experienced the highest year-over-year growth in H1 2025, rising by 17.6% and 16.1% to USD 13.4 Bn and USD 32.1 Bn, respectively. This trend reflects LPs’ growing preference for flexible, niche, and scalable investment opportunities. Conversely, mega funds (USD 5 Bn+) declined by 30.0% to USD 140.2 Bn, as investor caution increased toward high-value investments.

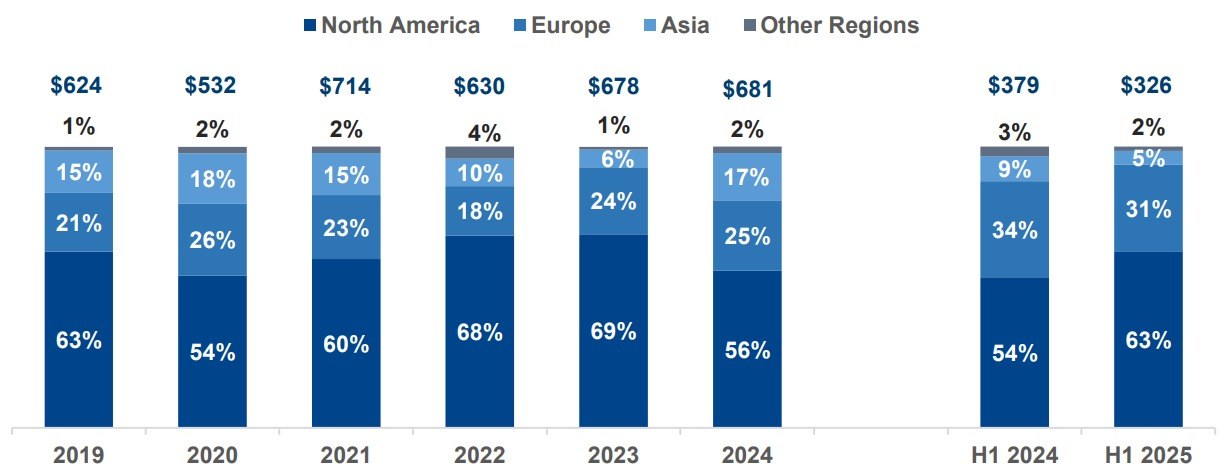

- Regional Shifts: PE fundraising in North America grew by 0.3% to USD 203.8 Bn in H1 2025, up from USD 203.1 Bn in H1 2024, while Europe and Asia saw declines due to geopolitical uncertainty and other regional challenges.

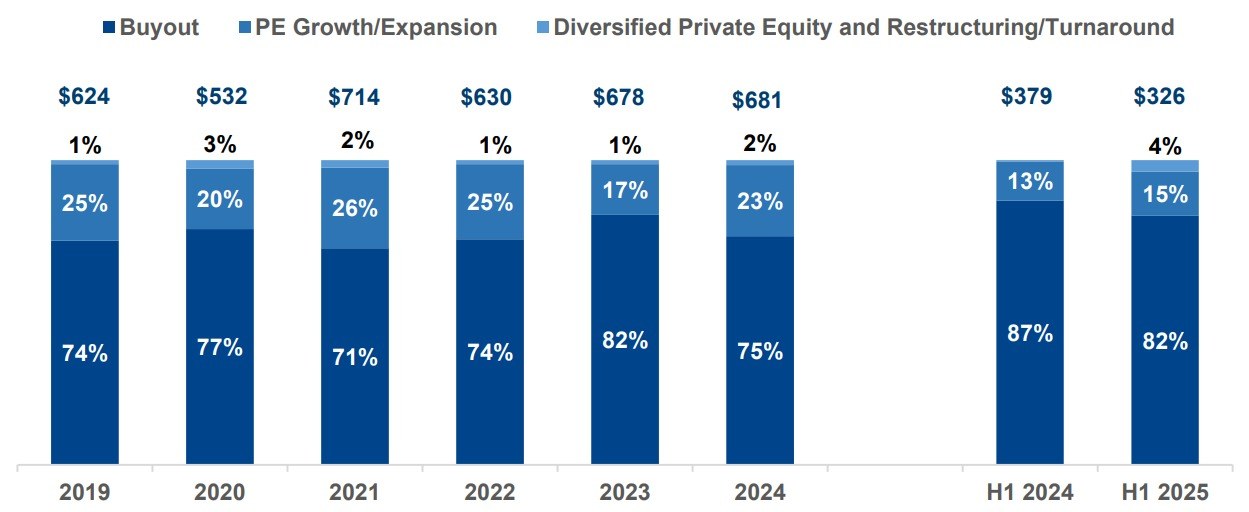

- Growing Preference for Alternative Strategies: Turnaround funds raised USD 12.3 Bn in H1 2025, up from USD 1.5 Bn in H1 2024. This growth was supported by LPs shifting their focus from traditional large buyout funds to alternative strategies that offer downside protection.

- Shortened Timeline: Fundraising durations declined from 17 months in H1 2024 to 13 months in H1 2025, reflecting investors’ preference for funds with shorter timelines and faster deployment cycles.

PE Fundraising Activity

In H1 2025, funds raised by PE firms declined by 14.0% in value and 1.4% in volume compared to H1 2024. High borrowing costs and delayed capital returns to LPs, driven by few exits, were key factors contributing to the decline. These challenges were further compounded by global tariff disputes and geopolitical tensions, which continued to dampen investor sentiment and constrain capital flows.

Fundraising by Fund Size

In H1 2025, small (under USD 500 Mn) and mid-sized (USD 0.5–1 Bn) funds recorded the highest year-over-year growth, rising by 17.6% and 16.1%, respectively. Small funds grew from USD 11.4 Bn in H1 2024 to USD 13.4 Bn, while mid-sized funds increased from USD 27.7 Bn to USD 32.1 Bn.

This shift in LP preferences toward flexible, niche opportunities, particularly in specialized sectors such as healthcare and technology, along with rising inflows from individual investors seeking flexible investment options, supported the growth of smaller funds. Mid-sized funds also benefited from steady deal activity, driven by add-on acquisitions and buy-and-build approaches.

In contrast, mega funds (USD 5 Bn+) declined by 30.0%, falling from USD 200.5 Bn to USD 140.2 Bn, as LPs grew more cautious about large-ticket commitments.

Fundraising by Region

In H1 2025, PE fundraising in North America rose to USD 203.8 Bn, marking a 0.3% increase from USD 203.1 Bn in H1 2024. Despite tariff concerns and market uncertainty in the US, LPs remained focused on long-term value creation and portfolio diversification. Growth was further supported by strong interest in resilient sectors such as infrastructure, renewable energy, and technology, along with the successful closing of several large funds led by experienced managers.

In contrast, fundraising in Europe declined by 21.8%, from USD 129.2 Bn in H1 2024 to USD 101.1 Bn in H1 2025, as weak economic growth and ongoing regional challenges dampened LP risk appetite, particularly in non-core markets such as Southern and Eastern Europe, where fundraising activity remained subdued.

Fundraising in Asia dropped sharply by 51.7%, from USD 33.7 Bn in H1 2024 to USD 16.3 Bn in H1 2025. This decline was primarily driven by a significant slowdown in China-focused fundraising, caused by weak domestic demand and uncertain government policies. Additionally, weak exit pipelines and increased regulatory pressure further weighed on investor confidence, prompting many LPs to scale back their commitments in the region.

Fundraising by Fund Type

Turnaround funds reached USD 12.3 Bn in H1 2025, up from USD 1.5 Bn in H1 2024. This sharp increase was driven by LPs shifting away from large buyout funds toward defensive strategies that provide improved capital protection.

Growth funds accounted for 15% of total PE fundraising in H1 2025, up from 13% in H1 2024. However, their overall value declined by 3.1%, from USD 48.9 Bn to USD 47.3 Bn, reflecting the broader market slowdown. The increase in share despite the decline in value signals LPs’ growing preference for lower-risk opportunities focused on strategic acquisitions and companies with strong organic growth potential.

In contrast, buyout funds saw a 19.0% decline in value, from USD 328.7 Bn in H1 2024 to USD 266.3 Bn in H1 2025. The drop reflects a shift in sentiment amid prolonged macroeconomic headwinds, elevated financing costs, and a slowdown in large-deal activity.

Private Equity Fundraising Duration (Months)

In H1 2025, the average fundraising duration declined to 13 months, down from 17 months in H1 2024. However, it remains elevated compared to pre-2022 levels, reflecting investor caution and selective capital deployment, which continues to weigh on fundraising momentum.

Top PE Funds

Largest PE Funds Closed in H1 2025 (By Fund Size)

| Fund Name | Fund Manager | Fund Size (USD Bn) | Fund Type | Region Focus | Available Dry Powder (USD Bn) |

|---|---|---|---|---|---|

| Ardian Secondary Fund IX | Ardian Secondary Fund (AXA) | 30.0 | Buyout | France | 28.5 |

| EQT XI | EQT | 26.1 | Buyout | Sweden | - |

| Advent International GPE XI | Advent International | 26.0 | Buyout | US | - |

| Blackstone Capital Partners IX | Blackstone Capital Partners | 21.0 | Buyout | US | 21.0 |

| Goldman Sachs Vintage X | Goldman Sachs | 17.5 | Diversified Private Equity | US | 14.2 |

| Insight Partners XIII | Insight Venture Partners | 10.0 | Buyout | US | 8.9 |

| Providence Strategic Growth VI | PSG | 6.0 | Growth/Expansion | US | 6.0 |

| Blackstone Energy Transition Partners IV | Blackstone Energy Partners | 5.6 | Diversified Private Equity | US | 5.2 |

| TowerBrook Investors VI | TowerBrook Investors | 5.6 | Buyout | UK | 5.4 |

| Oakley Capital Fund VI | Oakley Capital Private Equity | 4.8 | Buyout | UK | 4.8 |

| CVC Capital Partners Strategic Opportunities III | CVC Strategic Opportunities | 4.8 | Growth/Expansion | Luxembourg | 4.8 |

| Enfield Capital Partners Sports Fund | Enfield Investment Partners | 4.0 | Buyout | US | 4.0 |

| GTCR Strategic Growth Fund II | GTCR Strategic Growth Fund | 3.6 | Growth/Expansion | US | 3.6 |

| Olympus Growth Fund VIII | Olympus Growth Fund | 3.5 | Growth/Expansion | US | 3.5 |

| FTV VIII | FTV | 3.4 | Growth/Expansion | US | 3.4 |

| Ardian Expansion Fund VI | Ardian Expansion (AXA) | 3.3 | Buyout | France | 2.8 |

| ICG Europe Mid-Market Fund II | ICG Europe Mid-Market Fund | 3.2 | Buyout | UK | 3.2 |

Outlook

PE fundraising in 2025 is expected to stabilize and grow gradually following a challenging first half. The easing of interest rates and improving valuations are set to strengthen fundraising conditions and support capital flows. Furthermore, the investor base is broadening as small investors gain access to PE through wealth managers and specialized online platforms such as iCapital and Moonfare, enabling capital deployment beyond traditional institutional channels.

Regionally, North America is poised to lead the recovery, driven by mid-market deals and a supportive regulatory environment. At the same time, Europe is expected to rebound gradually, supported by growing interest in the technology and infrastructure sectors. In contrast, fundraising in Asia is likely to remain subdued due to regional instability, particularly tensions involving China.

The fundraising landscape is expected to favor mid-sized and smaller funds, which offer quicker deployment and faster returns. Meanwhile, mega funds face extended fundraising cycles amid cautious investor sentiment and elevated levels of dry powder, which have reduced appetite for immediate reinvestment. Overall, PE fundraising in 2025 will be shaped by firms’ strategic adjustments to the evolving market conditions and shifting investor preferences.

Ashwinkumar Pemmasani