2020 Stimulus Plans and Their Impact – Will These Be Enough?

Published on 09 Apr, 2020

The COVID-19 pandemic has disrupted supply chains globally and international trade, nearly shutting down the world economy. Looking at the current scenario, many renowned economists have predicted zero economic growth for 2020. Federal governments across nations are announcing unprecedented stimulus packages to deal with the downturn. While this will have a positive impact, the question is will it be enough, considering that two crises – economic and health – have fused into one, compounding the magnitude.

The pandemic, through its impact on people’s health, has affected the global economy. As you read this, likely in the comfort of your home, an increasing number of small businesses will be shutting shop, amid the debilitating effect on supply and demand. Countries across the globe are leaving no stones unturned in their fight against it.

The recession will likely surpass the recessions of the last two decades in both scale and duration. Not confined to any single sector (the 2008 sub-prime crisis impacted the financial sector, while the 2000-01 dotcom bubble affected internet-based companies), it has taken most industries in its grip. Despite governments acting swiftly and injecting monetary and fiscal stimulus, recovery will be difficult until the pandemic is over.

The table below depicts the measures taken by different countries to contain the outbreak and revive the economy.

Stimulus plans as a percentage of GDP (Updated as of April 5th, 2020)

Nations |

Total Amount($ Bn) |

Debt to GDP(%) |

Stimulus % of GDP |

|---|---|---|---|

US | 2,300 | 105% | 10.3% |

Germany | 808 | 61% | 20.3% |

UK | 406 | 84% | 14.9% |

China | 394 | 61% | 2.6% |

Spain | 220 | 98% | 15.3% |

Australia | 189 | 30% | 13.7% |

Canada | 57 | 85% | 3.1% |

Italy | 49 | 137% | 2.4% |

France | 49 | 100% | 1.8% |

Denmark | 46 | 28% | 12.8% |

Singapore | 42 | 112% | 11.4% |

India | 23 | 69% | 0.7% |

Japan | 4 | 237% | 0.1% |

Source: IMF, EuroStat, News Releases (Quartz)

The stimulus packages announced in 2020 dwarf the 2008 bailout ($700 billion by the US in 2008 versus $2.3 trillion in 2020). Some packages represent over 10% of the GDP for certain countries, which is significant. However, it would be difficult to draw a complete parallel as the 2008 bailout was aimed to save the corporate sector, big banks and financial institutions. It did not safeguard or aid taxpayers, who were also affected by the financial crisis.

Objective of stimulus

Prior to the COVID-19 outbreak, the IMF projected global growth at 2.5%; however, in the current situation, it is expected to drop to zero or negative.

|

“It is way worse than the global financial crisis of 2008-09.” - Kristalina Georgieva, Managing Director of the IMF |

The key factor behind the low growth is the declining purchasing power of consumers due to mass layoffs as businesses and services shut down, resulting in unemployment. While policymakers have taken measures to control the pandemic, they also realize the need to sustain the confidence of businesses and consumers. Nations across the world have devised various strategies such as tax incentives, loan guarantees, and wage subsidies to protect the interests of citizens as well as enterprises.

Measures taken by some of the nations are highlighted below:

The US

- Fiscal Tool: The Senate approved the largest economic stimulus package in recent times, the $2.3 trillion (around 11% of GDP) Coronavirus Aid, to provide assistance to individuals (including the unemployed), enterprises, and healthcare facilities.

- Monetary Tool: The Federal Reserve lowered the fed rate by 150bps to 0–0.25% It also introduced facilities to support the flow of credit, in some cases aided by resources from the Exchange Stabilization Fund.

Germany

- Fiscal Tool: Germany agreed to a package of $808 billion. A part of this will be financed through new borrowing; this underlines Berlin’s commitment to employ all possible resources in the fight against coronavirus.

- Monetary Tool: The ECB announced that it would purchase additional assets worth €120 billion ($130 billion) until the end of 2020 under the existing program.

The UK

- Fiscal Tool: The country unveiled an unprecedented £330 billion ($406 billion) loan scheme to support businesses through measures such as tax cuts, millions in grants and mortgage holidays.

- Monetary Tool: The steps include reducing lending rate by 65bps to 0.1%; expanding the central bank’s holding of UK government bonds and non-financial corporate bonds; and introducing a new Term Funding Scheme to reinforce the transmission of the rate cut.

China

- Fiscal Tool: The country approved a $394-billion package. Key measures include increasing spending on epidemic prevention and control; production of medical equipment; distribution of unemployment insurance; and implementation of tax relief measures.

- Monetary Tool: The government has injected liquidity in the banking system – ¥3 trillion ($0.42 trillion) in the first half of February and ¥20 billion ($2.83 billion) in end-March. In addition, the reverse repo has been lowered by 10–30bps.

While the numbers look promising, will this yield the desired results? Several aspects need to be looked at:

-

How would such huge bailouts impact fiscal deficit?

Sourcing funding for the packages would lead to an increase in fiscal deficit and debt levels for each country. Some of these nations already have debt to GDP ratio as high as 100%. Additional burden by way of stimulus will send it even higher.

The other way to look at it is that the funding is meant to support badly-hit sectors (such as airlines, travel & tourism) and the general public. The resultant increase in debt can be offset by recovering it from taxpayers when the economy returns to normal. If the country remains productive in the long-term and has healthy fiscal institutions, the taxes will not be a burden on people, and the federal government will not default on national debt either.

Reducing oil prices provides some cushion to oil-importing economies, such as India, where the government can control the fiscal deficit to some extent by not passing on the reduction in crude prices to consumers.

Overall, we feel a wider fiscal deficit would create problems largely for developing economies and countries with debt to GDP ratio above 100%; they may, therefore, take some time to recover. Separately, though, we think recovery will be much longer compared to that following the 2008-09 crisis. -

Are the packages enough for the $90-trillion world economy?

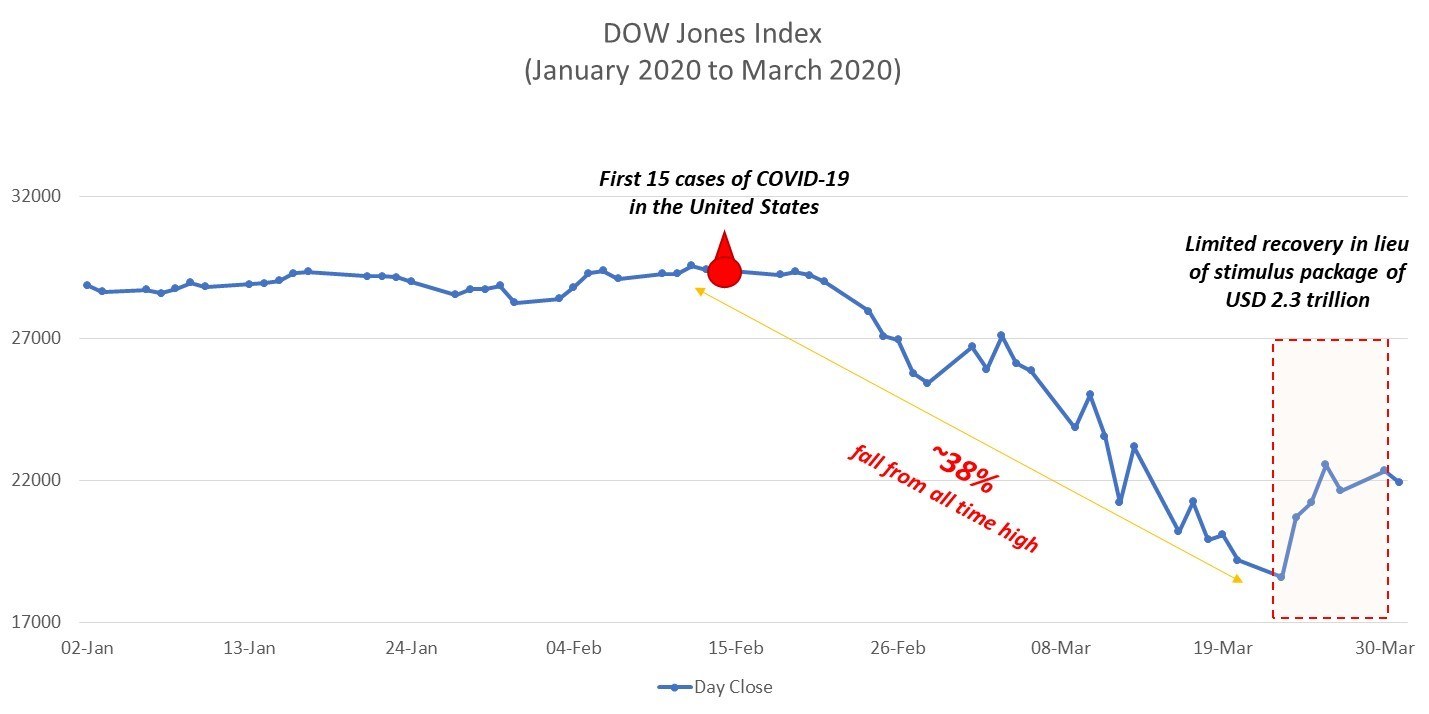

If we go by stock market as the barometer to assess whether the packages are enough or not, the investor sentiment is still negative. Dow Jones recovered only by 3,900 points after the announcement of bailouts. This indicates that worse is not over yet. Looking at numbers, the coronavirus confirmed cases in the US grew three times to 3,36,673 (April 5th, 2020) from 85,435 (March 26th, 2020), since the announcement of the stimulus package of more than $2 trillion.

G20 leaders have committed to do “whatever it takes” to minimize the social and economic impact of the coronavirus pandemic, in a largely unspecific and uncontroversial joint communique issued after a video conference call.

The size and type of package announced will help the economy in the short term, but if the negativity continues then there will be a need of more infusion. Recognizing the gravity of the situation, countries have pledged to provide additional financial support, if required. In a recent example, Singapore announced its third stimulus package of $3.6 billion on April 6th, 2020, taking the total to $41.7 billion.

Aranca View

Yes, the stimulus packages are huge and historic, but so is the scale of the pandemic that is yet to show signs of abatement. With the global economy at a standstill and governments extending lockdowns by a couple of weeks or even months, we believe additional bailouts are likely.

On the other hand, if countries manage to contain the spread of the virus in a couple of weeks (though it seems unlikely in the light of the increased number of confirmed cases and death) or an effective vaccine is discovered, the announced stimulus packages should be enough to take care of the economic downturn in the short term. However, this is a scenario we are hoping for; whether it will actually pan out the way we think, is highly doubtful.

Siddharth Jaiswal