From Tonnage to Technology: How South Korea Can Win the Specialty Engineering Polymer Race

Published on 03 Jul, 2026

For a generation, South Korea’s chemical industry competed the way its founders intended: on scale. Build the biggest crackers, run them hard, and sell the output into a China that could not buy fast enough. That model is now broken. A wall of Chinese capacity has turned the country from the world’s largest petrochemical buyer into its largest supplier, collapsing commodity margins and pushing South Korea’s producers, in 2025, to agree to shut up to a quarter of their cracking capacity.

But the same downturn has clarified where South Korea’s future lies. Demand across automotive, electronics, industrial and sustainability driven markets is migrating toward specialty engineering polymers, and in that arena the basis of competition is not tonnage but technology. The useful question is no longer how much South Korea can make, but whether it has what winning in specialty polymers actually requires. On most counts, it does.

The Game Has Changed

The commodity logic that built South Korea’s industry has quietly inverted. China’s ethylene capacity has climbed past 60 million tons with tens of millions more to come, and South Korean petrochemical exports fell more than 15% in a single recent year. No amount of operating efficiency closes a gap built on cheaper feedstock and deeper subsidies. Industry and government have read the signal the same way: the 2025 restructuring plan explicitly redirects the sector toward high value, environmentally friendly products.

Specialty engineering polymers are where that value sits. Unlike commodity resin, these materials compete on performance, certification and trust rather than price per ton, and demand for them is accelerating exactly where South Korea is strong. Electric vehicles now carry 200 to 250 kg of plastic each; electronics, already more than half of South Korea’s engineering plastics volume, is pulling specialty grades for 5G and advanced chips; hydrogen and industrial systems need polymers that survive extreme conditions; and regulators are mandating recycled content across all of them. The recycled engineering plastics market alone, already worth nearly USD 5 billion and led by Asia Pacific, is set to grow steadily as automakers and electronics brands chase recycled content targets. The demand is real. The open question is capability.

What Winning in Specialty Polymers Require

Strip away the chemistry and five capabilities separate the winners from the rest.

- The first is proprietary chemistry and IP, the grades competitors cannot simply copy.

- The second is qualification depth and stickiness: a specialty polymer is designed into a customer’s part over years, and once approved is rarely swapped out.

- The third is certified sustainability, the ability to prove recycled content and carbon footprint, now a condition of market access in Europe rather than a marketing claim.

- The fourth is integrated cost to serve: the feedstock and logistics position to deliver tailored grades reliably and economically.

- The fifth is market access, the tariff light routes into the buyers that matter.

These are not the levers of a commodity business, where scale and feedstock cost decide everything. They reward patience, R&D and relationships, and they are far harder for a subsidized newcomer to replicate. That is precisely why they favour an established producer, and why South Korea’s position is stronger than the gloom around its crackers suggests.

How Ready South Korea Is?

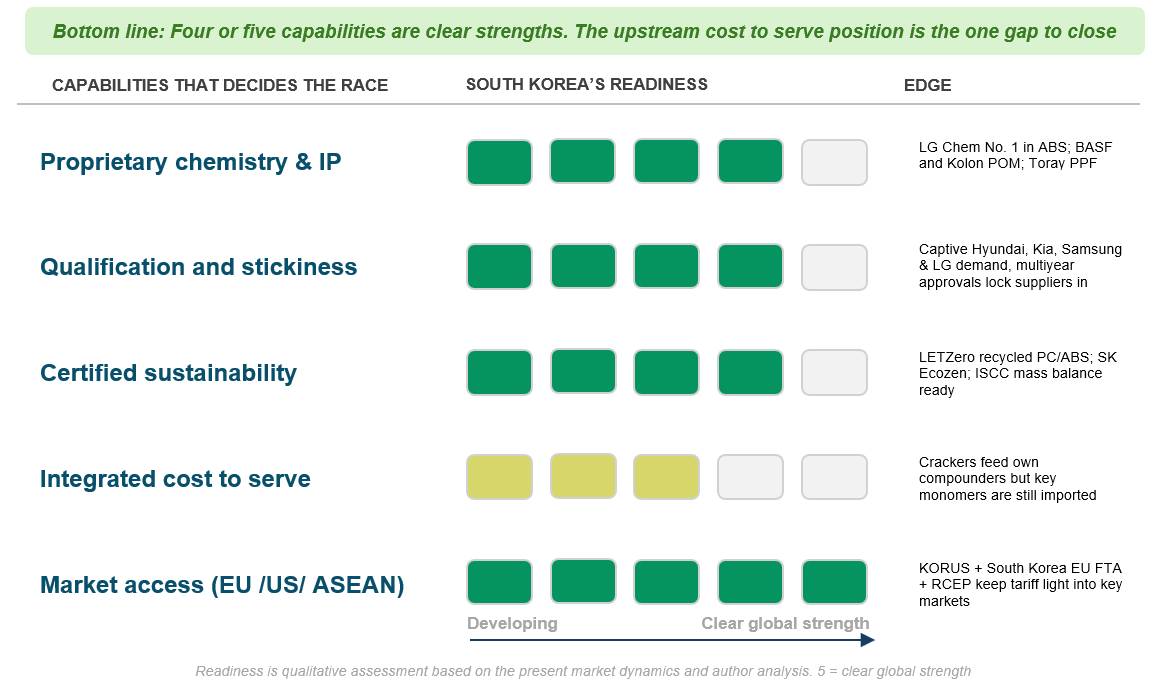

Measured against those five tests, South Korea starts from real strength. In chemistry and IP, LG Chem is the world’s No. 1 in ABS, the joint venture between BASF and Kolon runs one of the planet’s largest acetal plants, and Toray’s South Korean operations anchor high performance grades such as PPS. On qualification and stickiness, South Korean producers sit beside captive, demanding customers such as Hyundai, Kia, Samsung and LG, whose multiyear approval cycles, once won, lock suppliers in. On sustainability, the portfolio is unusually advanced: LG Chem’s LETZero recycled, flame retardant PC/ABS and SK Chemicals’ BPA free Ecozen copolyester already satisfy European rules competitors are still chasing. On market access, South Korea is close to best in class, with free trade agreements keeping its resin tariff light into the United States, the EU and ASEAN.

The one place South Korea is merely adequate is cost to serve, and specifically its upstream. The country’s specialty chains still lean on imported feedstocks and key monomers, a dependence that erodes both margin and resilience precisely when the two matter most. The direction of travel, though, is unmistakable: LG Chem has added polycarbonate capacity at Yeosu to feed the 800 volt platform of Hyundai and Kia, while Lotte Chemical is pushing compounding capacity toward 700,000 tons for automotive and electronics and aims to draw more than 30% of group earnings from specialty and battery materials by 2027.

Fig 2: South Korea’s readiness against the five capabilities that decide specialty polymer competition

How ready is South Korea to win in a specialty engineering polymers?

Closing the Gap That Matters

The constructive conclusion is that South Korea does not need to acquire new strengths so much as protect and extend the ones it has, while addressing a single structural weakness. Three moves follow. First, invest behind the chemistry, channeling the capacity freed by commodity closures, together with the government’s KRW 1.7 trillion materials programme, into super engineering and recycled grades rather than new tonnage. Second, turn sustainability into a product, not a compliance cost: mass balance and ISCC certification is something South Korean firms can sell to European OEMs racing to meet 2030 recycled content mandates. Third, shore up the upstream, where backward integration, recycled and biobased feedstock, and targeted partnerships can steadily reduce the import dependence that is the portfolio’s weakest link.

None of this asks South Korea to become a different industry. It asks it to finish a transition it has already begun, to compete on what its engineers do best rather than on a tonnage game it can no longer win.

Conclusion

The commodity downturn is painful, but it has done South Korea a favour by making the strategic choice unavoidable. The demand migrating toward specialty engineering polymers, from EV batteries to 5G antennas to hydrogen systems to recycled content rules, lands squarely on South Korea’s existing strengths in proprietary chemistry, customer trust, sustainability and market access. Close the one real gap upstream, and the country is not merely well placed to capture that demand; it is one of the few that can. The specialty polymer race will be won on capability, and South Korea is already most of the way there.

Vivek Gorle