Scaling Korean-Textiles in US and Europe via Sustainable Innovation

Published on 03 Jul, 2026

South Korea built one of the world’s most advanced fiber industries with global leadership in spandex, aramids, tire cords and recycled fibers, yet its textile and apparel exports have drifted sideways, squeezed between Japanese and German high-tech rivals above and low-cost Chinese and Southeast Asian volume below. Total textile exports sat near USD 11 billion in 2023, short of past peaks, even as the underlying technology base kept improving.

The opening, however, is no longer about cost. Two structural shifts such as Washington’s hardening line on Chinese-linked supply chains, and Brussels’ sweeping new sustainability rules are rewriting what “competitive” means in the world’s two richest apparel markets. For an exporter that already owns the high-value, sustainable and digital capabilities both markets are about to demand, the question is not whether to grow, but where in the value chain to concentrate.

Where South Korea Stands Today

A decade ago, South Korea’s textile story was one of slow, managed decline. The “nut-cracker” framing caught between more advanced economies and cheaper ones captured the mood, and it still describes commodity yarn and cut-make-trim apparel, where South Korean cost structures cannot match Vietnam or Bangladesh. The market is mature: roughly USD 30–34 billion domestically, with textile exports near USD 11 billion against an import bill closer to USD 19 billion.

But the picture at the high end is the opposite of decline. Hyosung is the world’s largest spandex producer with its Creora brand holding the global No. 1 position since 2011 and the long-standing leader in polyester tire cords. Huvis leads the world in low-melt fiber. Kolon and Hyosung sit inside the global top five in Aramids, alongside Teijin, DuPont and Toray. This is not a country lacking technology; it is a country whose best assets have been underpriced, because they were sold into a market that rewarded volume over value.

The Window is Opening: What Changed in the US and EU

The US shift is about provenance, not price. The Uyghur Forced Labor Prevention Act presumes that any good linked to Xinjiang origin of more than 90% of China’s cotton is made with forced labor and bars it from entry; US Customs had detained roughly USD 3.7 billion of shipments under the law by mid-2025. The 2025 termination of the de minimis exemption, plus tariffs on Chinese goods stripped the cost advantage from China’s e-commerce apparel model. Nearly 60% of US fashion companies now plan to source from more countries. South Korea with duty-free access under the KORUS free-trade agreement and no Xinjiang exposure is a natural beneficiary.

The EU shift is about data and durability. The Ecodesign for Sustainable Products Regulation, in force since 2024, identifies textiles as a priority category. A delegated act expected in 2027 will require a Digital Product Passport that carries information on material composition, carbon footprint, recyclability, and full supply chain traceability for every garment sold in the EU, regardless of origin. A ban on the destruction of unsold textiles is already being phased in. Compliance is becoming the price of market access and favors suppliers who can clearly demonstrate what their products contain.

Three Capabilities That Convert the Opening

South Korea’s own industrial strategy maps almost exactly onto what these two markets now reward. The 2024 Textile and Fashion Industry Competitiveness Strategy commit KRW 2.9 trillion and targets lifting South Korea’s share of the global industrial and eco-friendly textile market from 2–3% to 10% by 2030.

High value. Advanced industrial textiles such as aramids for ballistic and protective gear, carbon fiber, and marine fibers designed for extreme conditions are exactly the segments where demand from US defense and European industry is strongest. Demand for Aramids, where South Korea is a top five producer, is growing at high single digit to double digit rates toward more than USD 10 billion, and Toray’s South Korean arm is investing USD 365 million to expand aramid capacity in Gumi, reflecting strong confidence in the location.

Sustainable. Hyosung pioneered recycled nylon from ocean fishing nets in 2007 and was first in South Korea to win GRS-certified recycled polyester; its regen Ocean fiber cuts CO₂ by 73% and water use by 98% versus virgin nylon. Its partnership with California’s Ambercycle brings textile-to-textile circular polyester to South Korea. These are exactly the verifiable, document-ready inputs an EU Digital Product Passport will require.

Digital. South Korea is among the most digitally mature apparel economies, from the scale of Musinsa’s platform to government initiatives for AI driven design tools that can reduce development time by 80 percent and enable connected micro factories. This digital backbone also enables Digital Product Passport traceability to shift from a compliance cost into a service that South Korean suppliers can offer.

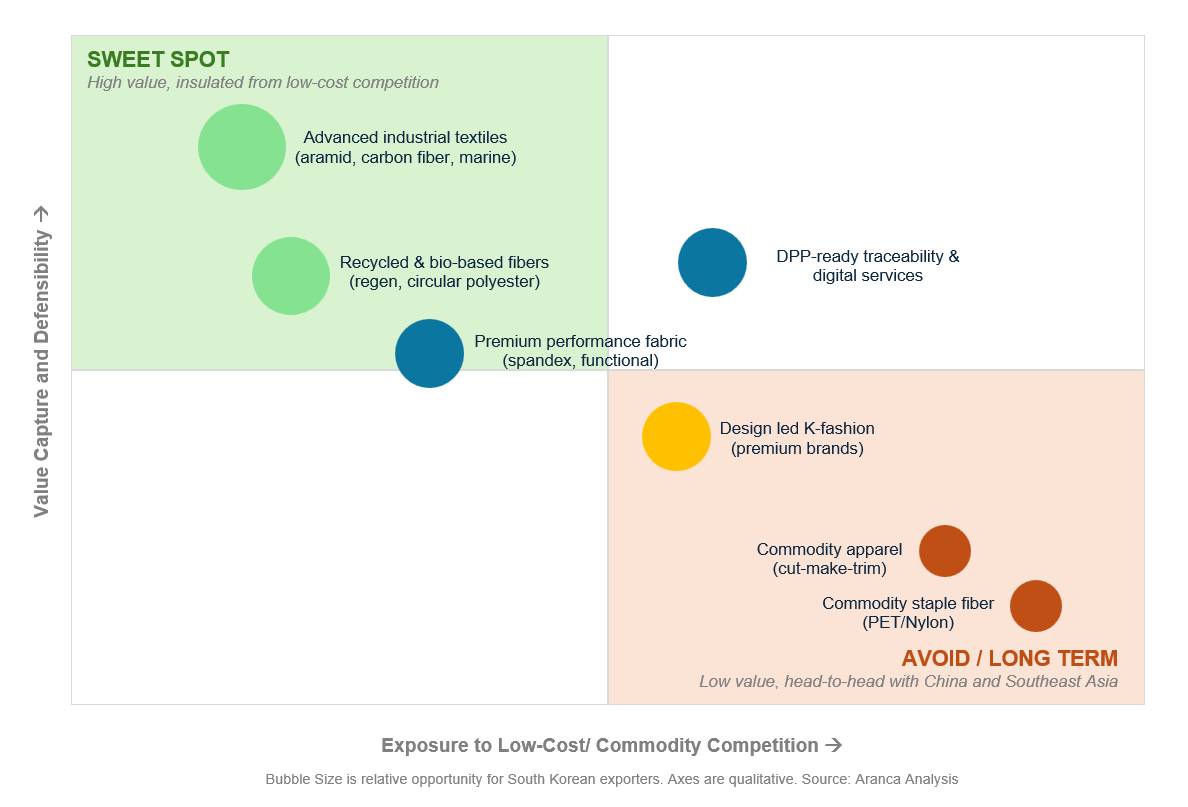

Fig 1: Where South Korea should concentrate. The upper-left “sweet spot” pairs high value with insulation from low-cost competition; the lower-right is where competing head-on with China and Southeast Asia destroys value.

Where South Korea Should Compete: A Value-Capture Map for Technical Textiles & Apparel

Where to Win

The map makes the choice explicit. The near-term prize is the upper-left: advanced industrial textiles and recycled or bio-based fibers, where Korea already holds IP, certifications and global leadership, and where US security demand and EU regulation create durable pull. Premium performance fabrics and emerging “DPP-ready” traceability services sit just behind, converting digital capability into a moat. Design led K fashion, backed by cultural momentum, is a real but trend dependent mid tier play. Commodity apparel and staple fiber form a volume base to defend, not a priority for new capital. The strategy aligns with other specialty sectors: use the commodity middle as a floor and move profits toward more defensible positions.

Conclusion

Korea’s technical-textile and apparel industry does not need to become something it is not. It already makes the high-performance fibers, the certified recycled materials and the digital infrastructure that the US and EU are, for the first time, structurally compelled to favor. The convergence is rare: a buyer base actively de-risking away from China, a regulatory regime that prices in sustainability and traceability, and a domestic supply base that happens to be strong in exactly those things. The exporters that win will be those that stop competing on price in the crowded middle and commit to the high-value, sustainable and digital ends where Korea’s advantage is real, and where, for the next five years, the door is open.

Vivek Gorle