The Cleaner Reaction: Reinventing the Water Industry with Green Chemistry

Published on 02 Jul, 2026

For over a century, water treatment has relied on chemical inputs such as metal salts, chlorine, and synthetic polymers to deliver safe and cost-effective outcomes, though often leaving behind sludge, harmful byproducts, and gaps in addressing emerging contaminants. Today, this model faces increasing pressure from stricter regulations, the rise of persistent “forever chemicals,” and the need to reduce energy Usage and carbon emissions. In response, industry is beginning to redefine water treatment by shifting toward cleaner, more sustainable approaches that use electrons, biological systems, and nature-based solutions to redefine how water is treated.

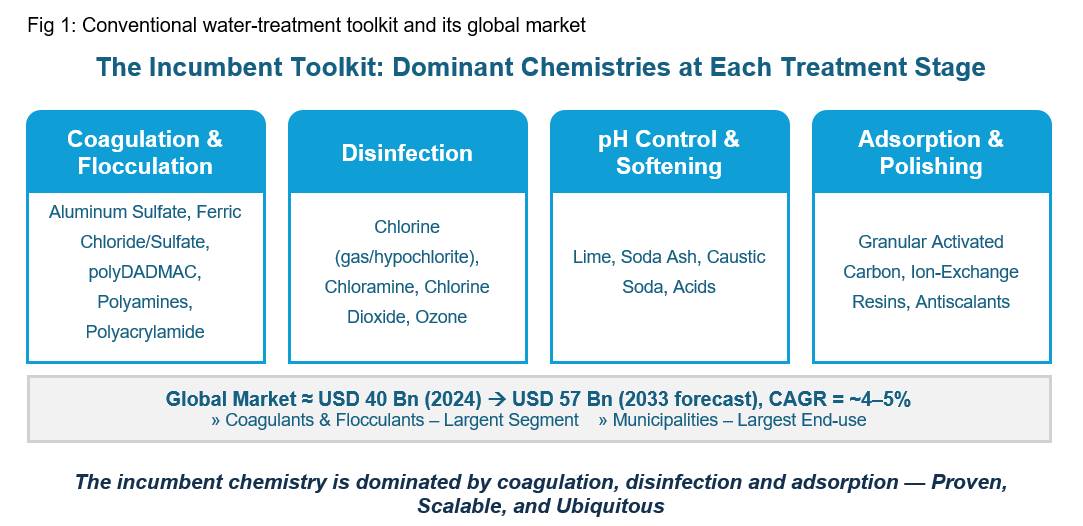

The Legacy Toolkit: Proven, Scalable, and Ubiquitous

Water treatment essentially involves four chemical processes carried out in the same order. Coagulation and flocculation come first and are the true workhorse: aluminum sulphate (alum) is the most widely used coagulant on earth, alongside ferric chloride and ferric sulphate, with organic coagulants such as polyDADMAC and polyamines and high-molecular-weight polyacrylamide flocculants used where reduced sludge is desirable. Disinfection overwhelmingly uses chlorine and chloramine. pH correction and softening rely on lime and soda ash and finally polishing on granular activated carbon and ion-exchange resin. This chemistry is mature and barely contested.

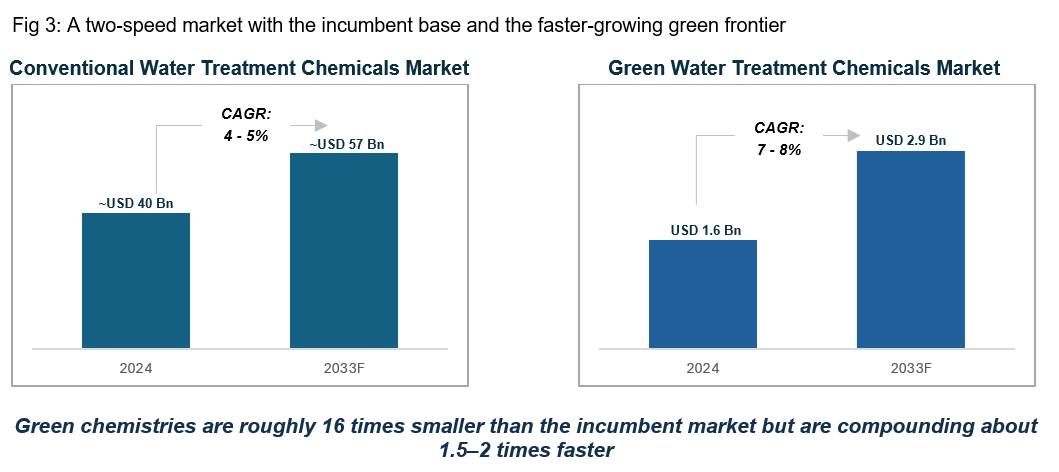

Enormous The scale is enormous. The global water-treatment chemicals market was about USD 40 billion in 2024 and is projected to reach roughly USD 57 billion by 2033, a growth rate of near 4-5%. Coagulants and flocculants are the largest segment, and municipal utilities the biggest end-users; in the US, over 90% of public water systems rely on coagulants. The supply base is concentrated among a few major players such as Kemira, Ecolab, Veolia, BASF, SNF, and Solenis, making the industry efficient but stubborn.

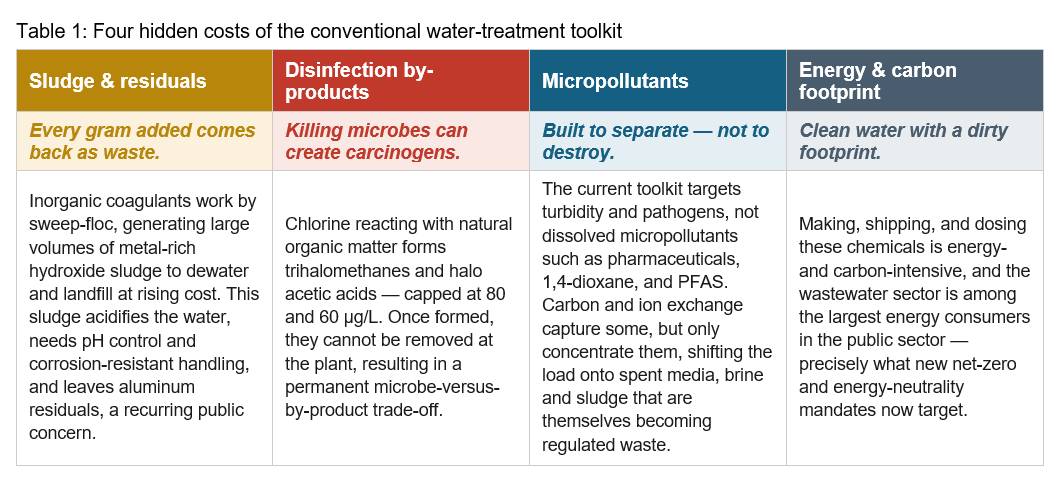

Hidden Costs of Current Water Treatment Solutions

The incumbent toolkit works, but each job carries a structural cost that has become harder to ignore. Four costs in particular are now actively reshaping the industry.

Regulatory Pressures the Incumbent Model Cannot Address

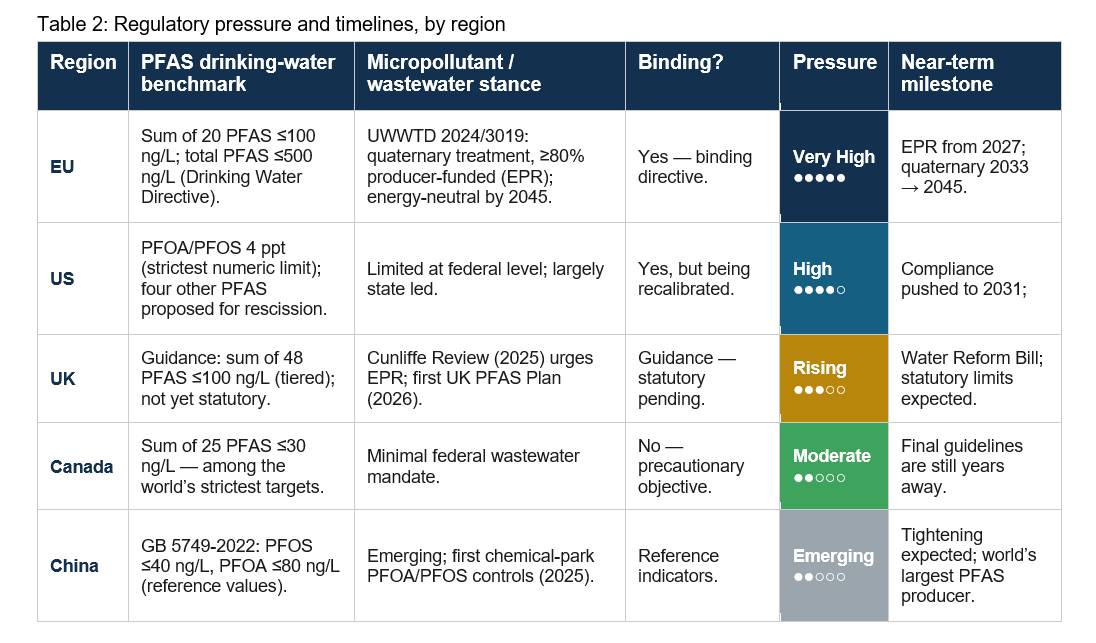

Regulatory pressure is converging on the gaps left open by the chemistry, but the pace is uneven globally. The table maps where regions stand and the timelines within which regulatory standards must be achieved.

Across markets, the challenge is consistent, even if the pace of change varies. Regulators are increasingly demanding the destruction of contaminants, reduction in chemical byproducts, and lower energy and carbon emissions, yet no single conventional solution can meet all three requirements. Europe is setting the systemic benchmark with binding, producer-funded rules on micropollutants, while the US enforces the most stringent limits, albeit across a narrower scope. The UK, Canada, and China are tightening regulations in parallel. This convergence of constraints is creating a clear opportunity for green chemistry solutions.

Enter Green Chemistry: Why Now?

Green chemistries either do the same tasks as traditional chemistries with biodegradable, low-toxicity inputs, or replace chemical dosing altogether with electrons, microbes and engineered ecosystems. Their rise is driven by four significant forces pulling in the same direction: 1) destruction-grade regulation (PFAS and micropollutants); 2) net-zero and energy-neutrality mandates; 3) the circular-economy logic of recovering energy, nutrients and reusable water from waste streams; and 4) disposal economics, due to the rising costs of sludge, brine and spent media. Crucially, “polluter pays” funding mechanisms such as Europe’s EPR are beginning to underwrite the capital these technologies require.

Green chemistry adoption is not a single rip-and-replace of the traditional chemistry pipeline but a strategic replacement depending on context: drop-in substitution where simple (bio-based coagulants for metal salts), bolt-on destruction in complex circumstances (electrochemical reactors for PFAS), and designed-ecosystem treatment in low-energy environments (constructed wetlands). The market reflects the transition from conventional to green chemistries: green water-treatment chemicals were worth about USD 1.5 billion in 2024 and are projected to reach roughly USD 3 billion by 2032. While it is still dwarfed by the incumbent market, this market is expanding at ~7%, well above the 4–5% growth of the conventional water-treatment chemical market.

Five Notable Green Chemistries: Advantages and Disadvantages

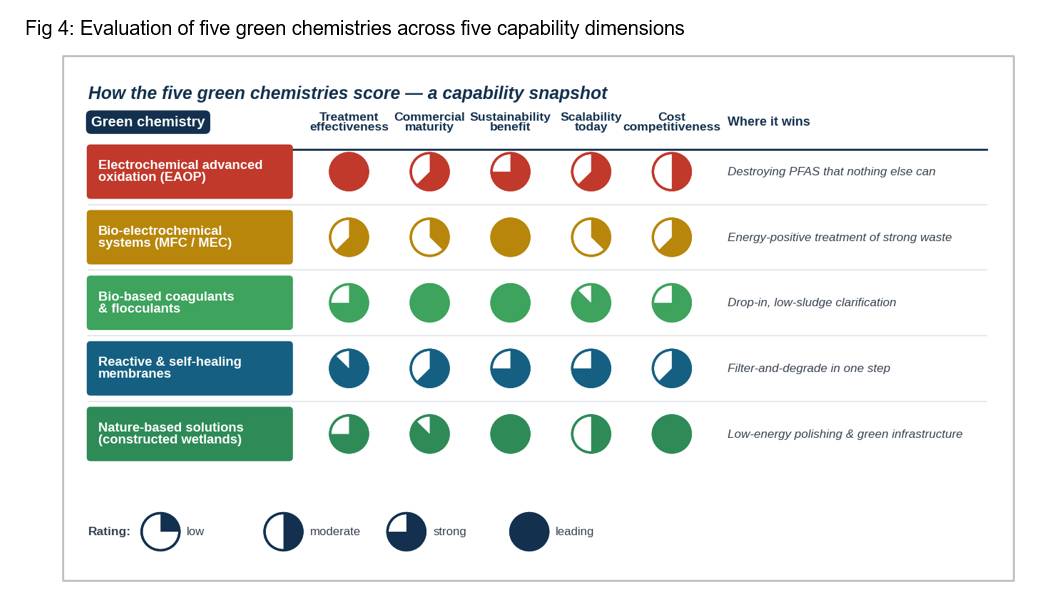

Given the broad and evolving landscape, the most relevant criteria for these technologies’ viability are proven deployment, commercial traction, treatment performance, and clear sustainability impact. Based on these criteria, five green chemistries are notable. These solutions vary significantly in maturity and application and are best viewed not as competing alternatives but as part of a complementary portfolio. The capability snapshot below evaluates each chemistry across five key dimensions, while the accompanying notes highlight their strengths and the remaining challenges they must address.

Electrochemical advanced oxidation process (EAOP) — the heavyweight. EAOP mineralizes pollutants and destroys PFAS outright (boron-doped-diamond anodes ~93% COD removal, electro-Fenton ~97% mineralization). The prime concerns are energy cost and electrode fouling, which are now mitigated with reduced-cost 3D electrodes and concentrate-then-destroy pipelines.

Bio-electrochemical systems — treatment that pays for itself. These turn organic load into electricity, hydrogen, or methane while recovering nutrients. While these are still pilot-scale due to removal stalling at low concentrations, they can be placed early in the pipeline and polish downstream.

Bio-based coagulants — the mature, drop-in option. These replace alum with biodegradable inputs and far less sludge (moringa up to ~90% COD/BOD cuts). The hurdle is feedstock variability, addressed with standardized extraction and hybrid formulations.

Reactive and self-healing membranes — filter and degrade at once. These membranes remove heavy metals and capture PFAS in a single pass. Fouling, a historic weakness, is now engineered out with self-healing coatings and AI fouling prediction.

Constructed wetlands — a designed ecosystem doing the chemistry. Near-zero energy and now an EU compliance route, with ~99% removal of BTEX, PAHs, phenol and metals in documented cases. Land area limits city use, so intensified vertical-flow designs and microbial-fuel-cell hybrids are used to extend their reach.

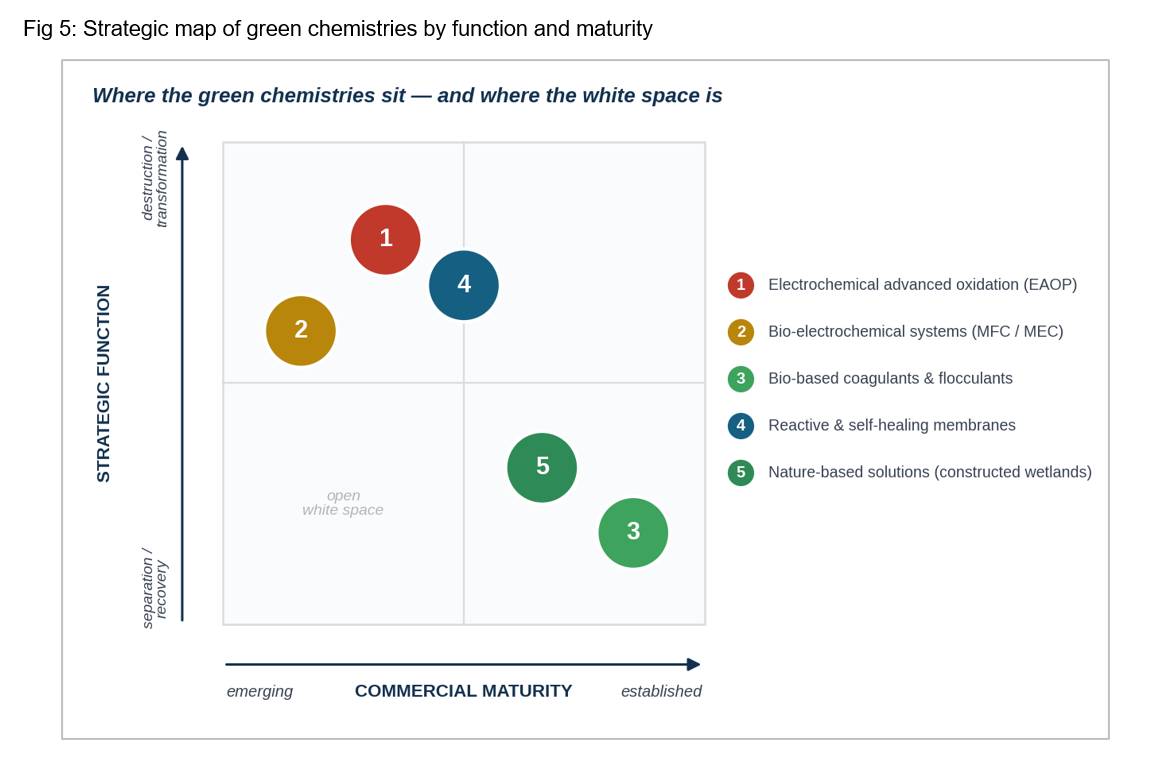

Mapping these five chemistries by strategic role and commercial maturity clarifies the landscape. Mature separation and recovery solutions such as bio-coagulants and wetlands are deployable today, supported by cost advantages and policy alignment. Electrochemical oxidation is emerging as the key scaling solution for contaminant destruction, while bio-electrochemical systems remain promising but nascent. Notably, few solutions focus solely on separation at an early stage, reflecting a shift in investment toward destruction and resource recovery.

Who Is Winning: Giants Reposition, Disruptors Specialize

The water-treatment chemical market sorts cleanly into four brackets depending on players’ actions, from incumbents deploying at municipal scale to specialists focused on PFAS destruction. The color-coded map below places eight of the most active players.

| Company | What they are doing | Recent developments | Plans & edge |

|---|---|---|---|

| TIER 1 · Full-service incumbents — own the customer and the treatment train | |||

| Veolia | Beyond PFAS, end-to-end: selective resins + GAC capture, plus high-temperature destruction. | $35m plant in Stanton, Delaware, US (2025), among the largest US PFAS systems; 33 live, 100+ planned (~2m people). | GreenUp €2bn; +50% green-solution sales by 2030; scale, services and disposal under one roof. |

| Ecolab (Nalco Water) | Digital + circular water: AI dosing, reuse and efficiency; biodegradable coagulant R&D. | Backed a PFAS-treatment technology via a $10m Emerald Ventures round (2025); growing AWS-certified sites. | Largest installed customer base; monetizes optimization, not just chemicals. |

| TIER 2 · Green-chemistry reformulators — biodegradable drop-ins at scale | |||

| Kemira | First biomass-balanced (ISCC+) bio-based polyacrylamide flocculants; activated-carbon reactivation for PFAS. | Superfloc BioMB deployed at Hamburg's largest WWTP; CuspAI AI partnership for PFAS removal. | #1 EU coagulants/polymers; renewable sales +15% in 2025, targeting €500m bio-based by 2030. |

| BASF | Readily biodegradable chelating agents — Trilon M (MGDA), Trilon G (GLDA, ~56% bio-based) — vs EDTA/NTA/phosphate. | Divested its mining flocculants business (Magnafloc) to Solenis in late 2024. | Chemistry depth; drop-in green substitutes for regulated legacy molecules. |

| TIER 3 · PFAS-destruction pioneers — own the hard reaction | |||

| Aclarity | Electrochemical PFAS destruction in modular reactors (Octa). | $15.9m Series A; mobile full-scale field reactors. | First-mover in validated, in-situ PFAS destruction across multiple verticals. |

| OXbyEL | Low-cost electrochemical oxidation reactors for PFAS and leachate. | Claims electrodes ~one-seventh the price of diamond anodes; utility and field pilots. | Cost-down economics aimed at making destruction affordable at scale. |

| TIER 4 · Capture & concentration specialists — feed the destruction step | |||

| BioLargo | Aqueous Electrostatic Concentrator (AEC): low-voltage electrostatic capture and concentration. | >99% PFAS removal incl. ultra-short-chain TFA, non-detect <1 ppt; ~1/40,000th the waste of carbon. | First commercial install (New Jersey, 2025); lowest-waste capture designed to feed destruction. |

| Puraffinity | Bespoke PFAS adsorbent media (Puratech) with low contact times for compact systems. | Validated and field-deployed; explicitly pairs with PFAS destruction partners. | Selective, compact capture from residential through municipal scale. |

Leadership variation based on metric. In terms of installed scale, financial strength, and the ability to deliver compliance at municipal volumes, Tier 1 and Tier 2 players remain unmatched. Veolia, for instance, is deploying PFAS treatment across over a hundred sites, while Kemira is advancing the use of biomass balanced flocculants at major European facilities. These incumbents continue to dominate in scale, reliability, and customer access.

However, at the frontier of contaminant destruction where long-term value is likely to concentrate, Tier 3 and Tier 4 specialists are leading with validated solutions for complex challenges that larger incumbents often outsource. Increasingly, major players are choosing to invest in and partner with these innovators rather than build such capabilities in-house, as reflected in moves by Ecolab and Kemira. The market is therefore likely to evolve into a bifurcated model, where incumbents retain control of customer relationships and treatment systems, while specialists own and commercialize the most advanced and difficult-to-replicate technologies.

Outlook: Shift to Hybrid, Modular, and Intelligent Solutions

The likely future is not a single winning technology but intelligent combinations of several complementary technologies, with each combination mitigating the weaknesses of one technology with the strength of another. Such combinations include:

- Concentrate-then-destroy trains that capture contaminants on a membrane or electrostatic concentrator and then mineralize them with electrochemical oxidation

- Wetlands wired with microbial fuel cells

- Electrocoagulation is paired with electro-oxidation

These combinations are likely to be reinforced by modular, decentralized units and AI that optimizes dosing and pre-empts fouling.

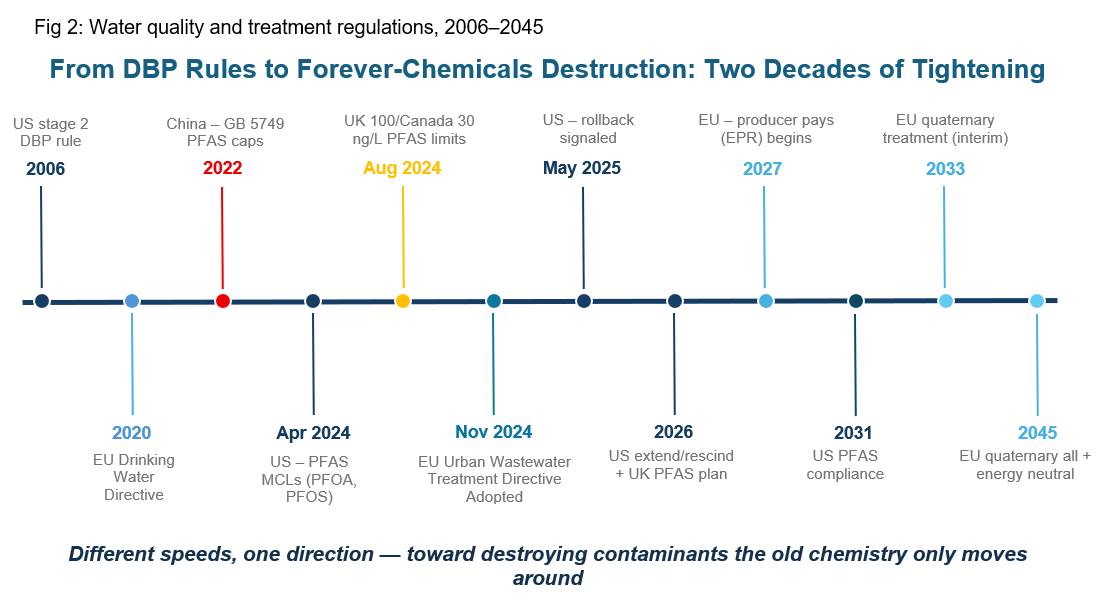

Green technologies timeline. Bio‑coagulants and PFAS capture‑and‑destruction technologies are expected to gain momentum by 2027, driven by US state regulations and producer‑funded mandates in Europe. From 2028 to 2033, interim deadlines for quaternary treatment in the EU will result in widespread implementation of advanced micropollutant removal across the region. Then, between 2033 and 2045, energy‑neutrality requirements will shift focus toward recovery‑oriented and nature‑based solutions. At this point, technologies that generate energy and recover resources rather than consume them will move from the periphery to the center of plant design.

Conclusion

Green chemistry is increasingly shifting from the periphery toward the core of water treatment, driven by tightening regulation, the emergence of contaminants beyond the reach of conventional methods, and growing pressure for polluters to bear the cost of pollutant treatment. The transition will be uneven: bio-based solutions will be adopted incrementally, while electrochemical approaches will scale more visibly, and most facilities will evolve toward hybrid treatment configurations rather than abrupt substitution.

What remains constant is the underlying industry logic. For decades, the response to water treatment was to add more chemistry through higher doses of coagulants, disinfectants, and polymers. The future will reward a fundamentally different approach. Competitive advantage will not come from adding more inputs, but from engineering cleaner, more efficient reactions that minimize residual impact while maximizing treatment effectiveness.

Vivek Gorle