Petrochemical Sector Reshuffle: EU’s decline opens door for Middle East and Asia

Published on 08 Aug, 2025

As the global petrochemical industry continues to face challenges, the EU petrochemical sector has faced intense pressures from persistent high energy prices, stringent regulations, and aging assets, causing ethylene plant operating rates to plummet to 70-75% in early 2024—well below global averages. Regulatory complexity and new chemicals legislation have further increased the costs of compliance and decarbonization, eroding competitiveness and forcing asset closures of 11 MTPA in last two years due to weak demand and unaffordable energy, leading to fundamental changes in the industry landscape. While the Middle East and Asia have added new capacity, global oversupply has depressed utilization rates and margins everywhere, prompting continued industry rationalization, consolidations, and closures. To regain competitiveness, the EU can focus on securing affordable energy, advancing decarbonization and circular economy strategies, simplifying regulation, and developing low-carbon chemical segments such as green ammonia—but recovery will be slower in the face of ongoing structural and regulatory headwinds.

Global petrochemical challenges

The global petrochemical industry faced a series of unprecedented challenges from 2020 to 2025 that reshaped its structure and outlook. The COVID-19 pandemic triggered a sharp decline in demand in 2020, with widespread supply chain disruptions and plant shutdowns. While 2021 saw a demand rebound, the industry continued to struggle with volatile feedstock prices and mounting environmental regulations. In 2022, new capacity – especially in Asia and the Middle East – outpaced demand, leading to oversupply, squeezed margins, and intensified global competition, particularly for naphtha-based producers.

The situation worsened in 2023 as geopolitical tensions majorly attributable to the Russia-Ukraine war spurred volatility in feedstock price, prompting plant closures in Europe and Southeast Asia. Margin pressures and consolidation trends extended into 2024, further impacted by China’s increasing self-sufficiency and regional overcapacity. Despite growing momentum for sustainability and circular economy initiatives, large-scale investments in recycling and low-carbon technologies remained limited due to high costs. By 2025, with a slow and uneven recovery underway, the industry began shifting its focus toward innovation, efficiency, and long-term resilience in a changing global landscape. The industry outlook seems challenging at least till 2026E. Here we present a summary on this trend.

Strain on EU Petrochemical sector

In the EU specifically, the petrochemical industry is battling high energy prices (natural gas costs remain 70% above pre-COVID levels), stringent environmental regulations, and aging infrastructure. These factors have impacted demand, with operating rates falling to 74% from more than 81% in 2022, and increased financial strain, prompting plant shutdowns and industry consolidation.

Weak demand and persistent oversupply

In early 2024, ethylene operating rates in Europe averaged 70-75%, well below the global industry expectation of 80-90%. This can be attributed to oversupply as global players increased capacities anticipating a spike in demand after COVID. However, a slow recovery in China, subdued global demand and China’s move toward self-sufficiency significantly impacted operating rates, leading to oversupply of chemical products in the global market.

High feedstock/input cost

Geopolitical risks, followed by sanctions on Russia, created a demand-supply gap, which spiked input costs for the EU region. This forced the EU to seek alternate energy sources. Thereby, EU’s dependence on Russian gas significantly declined, with volumes imported falling from 150 bcm in 2021 (45%) to 52 bcm (19%) in 2024. According to the European Commission, the roadmap is to gradually end imports from Russia by 2027. Presently, Norway, the US and Algeria are top exporters of natural gas to EU, accounting for 33.6%, 16.7% and 14.1%, respectively of the total EU’s gas imports.

Regulatory burden

The EU petrochemical sector is currently governed by a complex and evolving set of regulations aimed at enhancing competitiveness, sustainability, and safety. In July 2025, the European Commission announced an Action Plan for Chemicals that includes risk-based controls for chemical imports and increased international cooperation to secure critical chemical supply chains. The plan also addresses decarbonization, offering guidelines to support emission cost compensation and simplified environmental permitting for low-carbon projects. A revision of REACH (Registration, Evaluation, Authorization and Restriction of Chemicals), the cornerstone EU chemicals law, is expected by the end of 2025. This aims to streamline requirements and clarify procedures. However, experts continue to warn that high regulatory and compliance burdens, coupled with energy and carbon costs, pose a significant threat to the competitiveness of EU’s petrochemical sector.

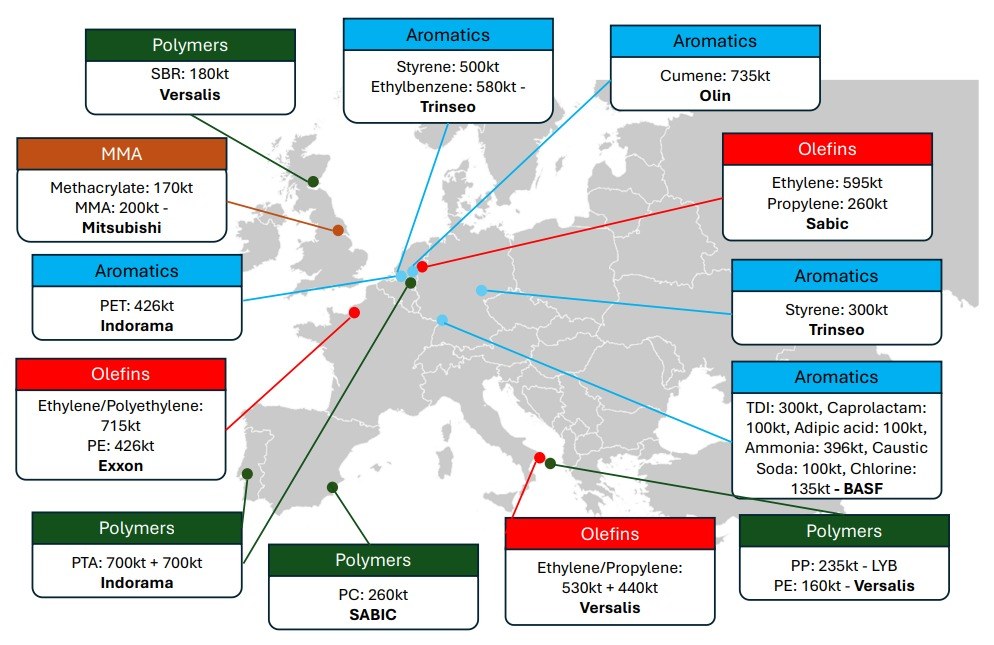

Asset closures

In 2023 and 2024, European chemical companies announced closures of more than 11 MTPA of production capacity across 21 major sites. An estimated 8-10% of EU’s steam cracking capacity has been closed since 2021 with a potential to reach 20% share of 2021 capacity. In 2025, Westlake’s Pernis plant shut its bisphenol-A and epoxy resin units with 250,000 tons of annual capacity as did INEOS’s Gladbeck facility, Europe’s largest phenol plant, with 650,000 tons of annual capacity of phenol and 409,000 tons annual capacity of acetone. These shutdowns are driven by persistent overcapacity, high energy and regulatory costs, and weak market demand, fundamentally reshaping the sector’s footprint in the EU. The following image shows capacity shutdowns in Europe in 2023-24.

Source: Cefic and Advancy report 2025

Key beneficiaries

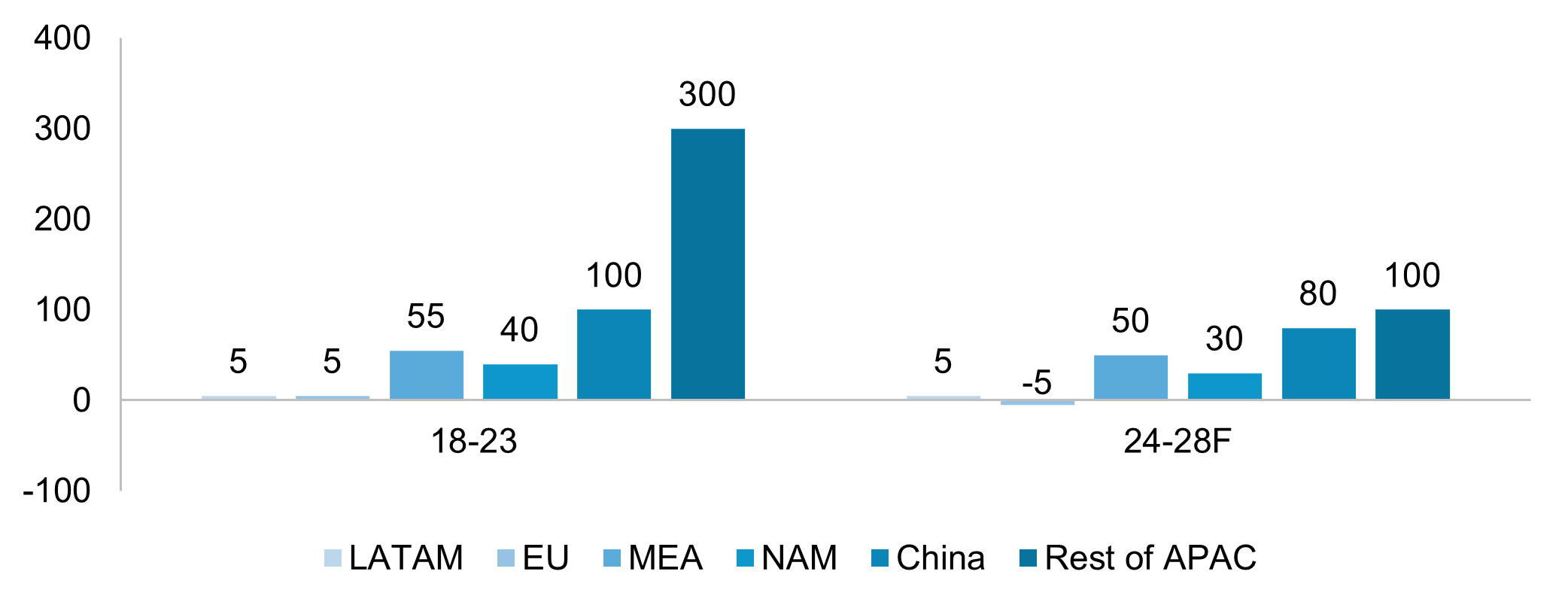

Seeing the challenges faced by the EU petrochemical sector, other regional players are adding or expected to increase capacity with major additions in the Middle East, China and Rest of Asia. However, due to comparatively less demand in these regions, utilization rates are expected to remain at 74-78% till 2027.

Source: Cefic and Advancy report 2025

Recent trends show continued rationalization and consolidation, with several major companies announcing plant closures, job cuts, and mergers or acquisitions to optimize their portfolios. For example, in 2025, Shell is exploring the sale of its European chemical assets. Meanwhile, joint ventures such as LyondellBasell and Covestro have permanently closed production units in the Netherlands due to high costs and weak demand. Consumption of key feedstocks like LPG is expected to decline across the petrochemical sector in Europe, further highlighting the ongoing challenges.

Capacity additions announced

Saudi Arabia: Tasnee National Industrialization Co. plans a new petrochemical complex in Jubail with an annual capacity of up to 3.3 million mt, including a world-scale ethylene cracker and downstream units for polyethylene (PE), MTBE, and specialty chemicals. The company targets a late-2030 start-up, pending completion of feasibility and engineering studies.

Saudi Arabia: Sahara International Petrochemical Co. and LyondellBasell aim to form a joint venture to develop a similarly sized mixed-feed cracker as Tasnee and a derivatives complex in Jubail. Preliminary plans call for annual capacities of 1.5 million mt of ethylene and 1.8 million mt of high-value polymer products. Feedstock approval from the Saudi energy ministry paves the way for a full feasibility review.

UAE: Abu Dhabi National Oil Company (ADNOC) and OMV unveiled plans to combine Borouge plc and Borealis AG into a new entity called Borouge Group International by the first quarter of 2026. As part of the agreement, ADNOC will acquire North American polyethylene producer Nova Chemicals for USD13.4 billion.

China: Refining capacity in 2024 stood at 955MTPA. China expects to add another 25-30 million tons of refining capacity in the next 2-3 years. Several players have already announced expansion plans – majorly in cracking capacities for ethylene production.

Aranca’s View: Options for EU to retain its lost share

Secure affordable and reliable energy supply

The EU seeks to implement the Affordable Energy Action Plan launched in February 2025, which will help reduce high feedstock and energy costs that currently undermine European producers. It would also ease financial pressure and support decarbonization projects through streamlined permissions and better grid access for electrification.

Drive decarbonization and circular economy transition

The EU aims to promote investments in low-carbon technologies, alternative clean feedstocks (biomass, recycled waste, carbon capture), and scale-up of circular solutions, supported by EU funds such as Horizon Europe, the Innovation Fund, and a forthcoming Industrial Decarbonization Bank targeting up to EUR100 billion. Additionally, CCUS technology should ideally be implemented to assure regulatory compliance.

Explore partnerships with leading players

We expect partnerships with the industry’s key players that are exploring or already have a presence in low-carbon technology/products to help EU players remain competitive. Players such as SABIC, the ADNOC group, etc., have announced plans to create a few products that include green and blue ammonia, sustainable aviation fuel (SAF), green hydrogen, etc.

Capture share in low carbon ammonia

As the petrochemicals industry shifts focus toward low-carbon chemicals driven by regulatory requirements, one of the key nitrogen fertilizers – ammonia – is gaining traction. Ammonia can be produced with low carbon emissions. According to the International Fertilizer Association (IFA), green ammonia capacity of 1.3MTPA is expected to be commissioned in the EU in 2025, with an additional 5.3MTPA capacity to be added by 2028. We believe EU players have an opportunity to build presence, which will help the EU regain its share in the global market and also abide by regulatory requirements.

In essence, petrochemical products are essential and will continue to remain key products essential for daily use. However, the EU’s faces challenges both in terms of structural obstacles and global conflicts. Most of these can be addressed by adhering to EU regulatory requirements that require investment in facilities adapting low-carbon emission plans, procuring input material from low-cost alternate sources and partnering with leading players to re-establish presence in the EU petrochemical industry.

Dharmik Patel