Consumer Non-durables in US Brace for Tougher Times as Economic Rampage Continues

Published on 16 Jun, 2020

The COVID-19 crisis is not likely to get over anytime soon. Several countries have already declared their economies are in recession. Sectors like consumer non-durables have been adversely impacted as the purchase of non-essential items has completely stopped. With lockdowns disrupting supply and demand declining, there seems to be no respite for the sector in the near term.

The speed and scale of the COVID -19 crisis has shocked even the most powerful and developed nations. The global economy has not seen a health crisis of such magnitude in the last 75 years. As of May 29th, 2020, the number of infections world-wide topped 5.9 million and the death toll was above 0.3 million and still rising. The global recession is slowly becoming a reality as countries across are struggling with complete shutdown of most business activities.

The US currently has 0.2 million patients and the country’s economy should brace for a challenging period ahead. The global rating agency Moody’s quoted that the spread of coronavirus will adversely impact a modest portion of North American corporates. Additionally, the government plans of COVID-19 containment like widespread lockdowns has evident downside risks to various sectors including consumer non-durables such as apparel and footwear.

Consumer spending constitutes approximately two-thirds of the total GDP in the US. As the virus spreads unabated in the country, sales of non-essential items have almost reduced to negligible. However, non-durable companies supplying frozen food and everyday essentials have benefitted from panic-buying following the outbreak. The positive trend notwithstanding, consumer spending is going to be low during the first half of the year and consumer non-durables stand to take a severe hit.

Recent data shows that retail sales in the US slid 16.4% in April 2020 from that the previous month. Of this, the largest decline was recorded in sales of clothing and accessories (down 78.8% MoM), and electronics and appliances (down 60.6% MoM).

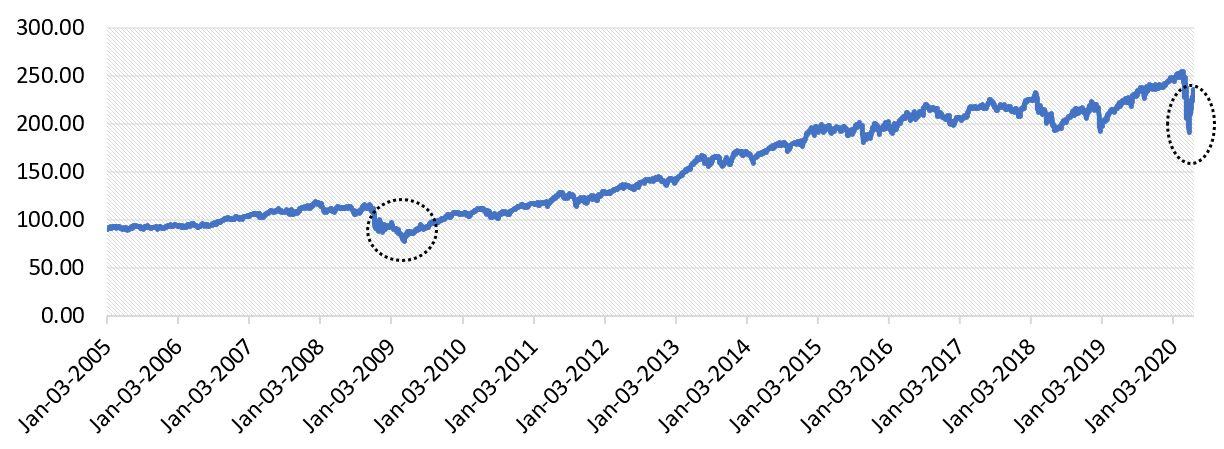

To understand the trend better, it is important to compare the current performance of the consumer non-durable sector with that during the recession of 2008-09. This can be gauged from the chart below that depicts the performance of the MSCI US consumer staples index.

MSCI US Consumer Staples

*circled area shows slowdown period

Source: Cap IQ, Aranca

Despite the slowdown during both periods, the index is around 119% up in May 2020 from its low in 2008-09.

Consumer behavior during 2008 recession versus COVID-19 situation

2008 Great Recession |

2020 COVID-19 |

|

|---|---|---|

Consumer Behavior |

|

|

Consumer Attitude |

|

|

Macroeconomic Sentiment |

|

|

High-demand Products |

|

|

Low-demand Products |

|

|

Sector-wise impact of COVID-19 on non-durables

Apparel and footwear

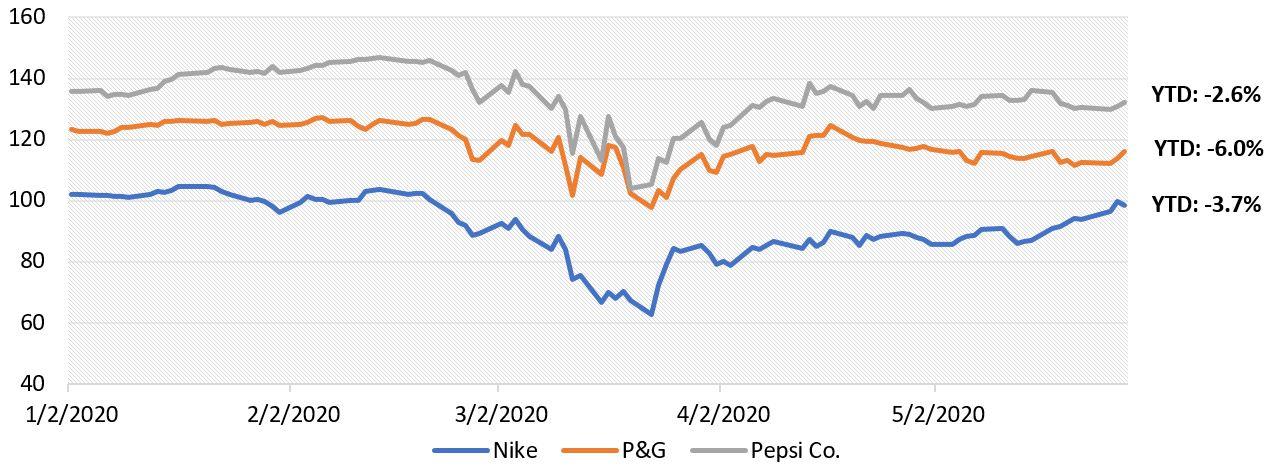

This is one of the industry’s worst affected by the COVID-19 crisis. The US government has issued directives on shutting down many manufacturing plants to contain the spread of the virus. Additionally, on the demand side, consumers would cut down expenditure on non-essential items like clothing and footwear. This is evident in the YTD performance (as of May 28, 2020) of some of the biggest companies (by market cap) in the industry. On YTD basis, Nike’s returns stood at -3.65%, while Columbia Sportwear Co’s. plummeted 26.78%.

Alcoholic and non-alcoholic beverages

So far in the pandemic-driven crisis, the impact on the sale of alcoholic beverages has been uneven. While some players recorded a surge in sales, others saw a decline. Economy spirits outsold luxury, super-premium and ultra-premium liquors. However, in terms of performance, YTD returns of almost all stocks are in red.

Non-alcoholic beverages are facing significant challenges due to the outbreak of COVID-19. Few companies such as Coca Cola are dealing from supply side disruption as it sources artificial sweetener from China.

Food-diversified

Consumer food companies are tackling issues such as decreased consumption and supply chain disruption. While the direct effect on the food industry will be felt as long as the pandemic lasts, any largescale impact is highly unlikely.

Household/personal care

The household and personal care industry is known to be resilient to economic changes. In this case, consumers in most countries affected by the virus began stockpiling essential household items. Specifically, demand for paper-based products has surged. However, significant supply disruption can be experienced if the lockdown in infected countries continues for a longer period.

Anticipated impact on consumer demand industry-wise

Category |

Consumer Behavior |

Impact |

|---|---|---|

Personal care essentials: Handwash, sanitizers, paper napkins, disinfectants, etc. |

| Positive |

Emergency essentials: Toilet paper, feminine hygiene products etc. |

| Positive |

Food staples with higher shelf life: Cereals, canned food items, etc. |

| Positive; however, sales may dip in the near term as condition stabilizes |

Snacks: Chips, cookies, etc. |

| Positive |

Frozen foods: Vegetables, meat, ice cream, etc. |

| Positive; however, lower impact than the two categories mentioned above |

Daily use essential food items: Milk, eggs, other dairy products |

| Positive |

Flours and sugar |

| Positive |

Farm produce: Fruits, fresh vegetables, etc. |

| Positive |

Non-alcoholic beverages: Soft drinks, juices, etc. |

| Positive |

Alcoholic beverages |

| Mixed |

Apparel and footwear |

| Negative |

Stock performance of highest revenue earners sector-wise (Currency in USD)

The performance of the top earning stocks is in line with consumer behavior. PepsiCo Inc. is the least impacted of the three, with YTD performance at -4.2%. Nike’s returns are the lowest among the three.

Top picks based on profitability and credit strength

Household and personal care

Company Name | Total Revenue [LTM] (USD mm) | EBITDA Margin % [LTM] | Net Debt | EBITDA | FCF | Finance Cost | Net leverage (x) | EBITDA Coverage (x) |

|---|---|---|---|---|---|---|---|---|

The Procter & Gamble Company (NYSE:PG) | 69,594.0 | 26.9 | 22,786.0 | 18,749.0 | 12,951.0 | (450.0) | 1.2 | 41.66 |

Kimberly-Clark Corporation (NYSE:KMB) | 18,450.0 | 21.3 | 7,738.0 | 3,936.0 | 1,527.0 | (261.0) | 2.0 | 15.08 |

The Estée Lauder Companies Inc. (NYSE:EL) | 15,853.0 | 22.1 | 4,272.0 | 3,498.0 | 1,756.0 | (134.0) | 1.2 | 26.10 |

Colgate-Palmolive Company (NYSE:CL) | 15,693.0 | 25.5 | 7,577.0 | 4,005.0 | 2,798.0 | (192.0) | 1.9 | 20.86 |

Food and beverage

Company Name | Total Revenue [LTM] (USD mm) | EBITDA Margin % [LTM] | Net Debt | EBITDA | FCF | Finance Cost | Net leverage (x) | EBITDA Coverage (x) |

|---|---|---|---|---|---|---|---|---|

PepsiCo, Inc. (NasdaqGS:PEP) | 67,161.0 | 18.7 | 27,890.0 | 12,579.0 | 5,417.0 | (1,135.0) | 2.2 | 11.1 |

Archer-Daniels-Midland Company (NYSE:ADM) | 64,656.0 | 3.99 | 9,065.0 | 2,580.0 | -6,280.0 | (402.0) | 3.5 | 6.4 |

Tyson Foods, Inc. (NYSE:TSN) | 43,027.0 | 9.55 | 11,749.0 | 4,110.0 | 1,286.0 | (483.0) | 2.9 | 8.5 |

The Coca-Cola Company (NYSE:KO) | 37,266.0 | 32.2 | 32,991.0 | 11,990.0 | 8,417.0 | (946.0) | 2.8 | 12.7 |

Footwear and apparel

Company Name | Total Revenue [LTM] (USD mm) | EBITDA Margin % [LTM] | Net Debt | EBITDA | FCF | Finance Cost | Net leverage (x) | EBITDA Coverage (x) |

|---|---|---|---|---|---|---|---|---|

NIKE, Inc. (NYSE:NKE)* | 41,274.0 | 14.4 | 3,474.0 | 5,860.0 | 3,426.0 | (124.0) | 0.59 | 47.26 |

V.F. Corporation (NYSE:VFC) | 14,313.9 | 16.4 | 2,952.8 | 2,345.2 | 812.49 | (89.7) | 1.26 | 26.14 |

Ralph Lauren Corporation (NYSE:RL) | 6,391.4 | 15.6 | 914.0 | 996.5 | 584.20 | (17.9) | 0.92 | 55.67 |

Skechers U.S.A., Inc. (NYSE:SKX) | 5,242.5 | 12.0 | 341.4 | 630.0 | 190.45 | (7.5) | 0.54 | 83.99 |

Conclusion

Most non-consumer durable companies in the US are working with a sense of urgency as they look to ensure safety of employees as well as meet the requirement of consumers. They are also struggling to keep products high in demand on shelf, despite challenges related to production and supply disruption. There is no certainty about when things will normalize in the US and globally. Regular production and supply chain operations are not likely to resume before 2–3 months. Food, beverage and essentials are not likely to be impacted significantly, as their existing stock is sufficient to meet demand in the market over this period, until of course supply diminishes. However, apparel and footwear are expected to bear the brunt of the COVID-19-induced recession.